Analysis of the German insurance market based on the Solvency ratios of 300 solo insurers that have published figures between 2016 – 2023.

The chart below highlights the ratio shift over the years.

The distribution of the SCR (Solvency Capital Requirement) of 320 insurers in 2023 is broadly concentrated around EUR 100 million, higher than the full European market for the entire period.

In contrast the EOF (Eligible Own Funds to meet the SCR) are more closely aligned with the historical data, concentrating closer to the EUR 1 billion mark.

Further 2023 SFCR analysis from Solvency II Wire Data

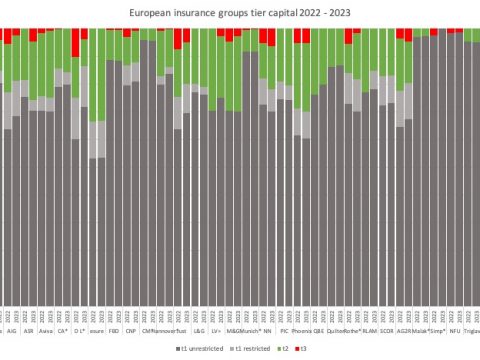

Distribution of group SCR and MCR ratios of European insurers 2016 – 2023

UK Solvency ratio distribution 2016 – 2023

Insurance asset allocation of Europe’s largest groups 2016 – 2023

SFCR 2023: Solvency II template S.25.05 partial and full internal model reporting

European insurers that halved their solvency ratio in 2023

AXA Group reports highest Solvency II ratio to date

More information about the data is available to premium subscribers of Solvency II Wire Data and subscribes to Solvency II Wire‘s exclusive SFCR Spotlight mailing list (subscribe for free here).

Datasets available on Solvency II Wire Data

-

- Swiss Solvency Test (SST): all available data 2016 – 2023

-

- Bermuda Financial Conditions Reports (BSCR): all available data 2016 – 2023

-

- Bermuda Financial Statements: data for 226 insurers 2016 – 2023 (1324 reports) selected tables

-

- Israel Economic Solvency Ratio Reports: all available data 2016 – 2022

-

- Lloyd’s Syndicate filings: data for 143 syndicates 2016 – 2023 (872 reports) selected tables

-

- SOLVENCY II WIRE DATA Captive Hub