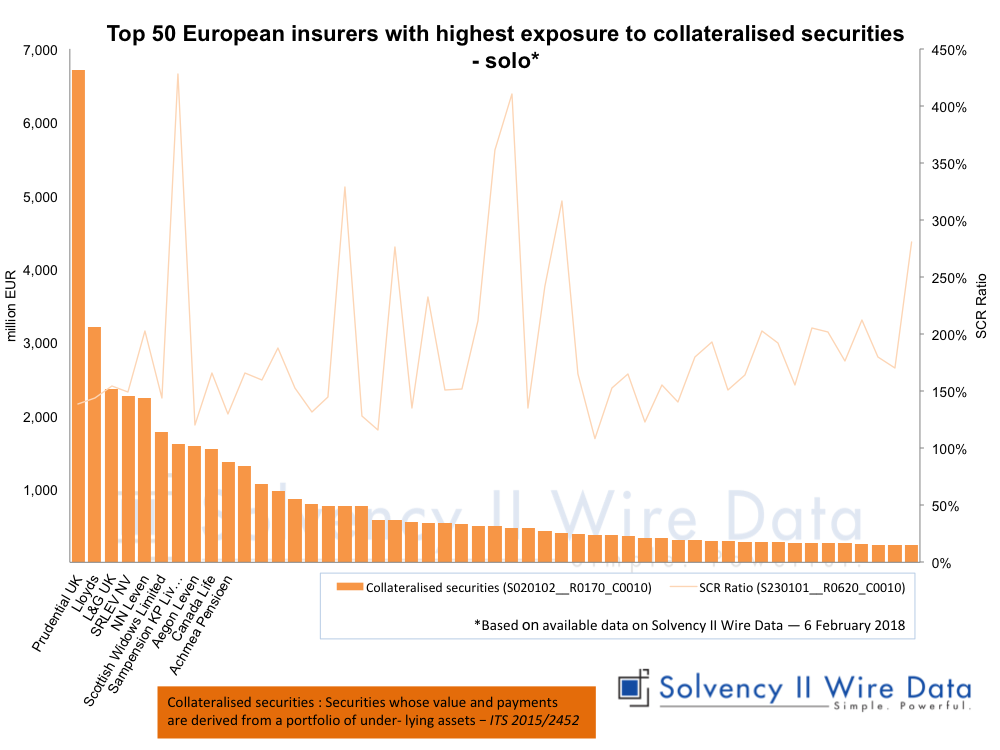

Chart title: Top 50 European insurers with highest exposure to collateralised securities – solo

Description: List of 50 solo European insures with highest exposure to collateralised securities on their balance sheet (Solvency II balance sheet).

Definition: collateralised securities, ITS 2015/2452, page 54

Securities whose value and payments are derived from a portfolio of under lying assets. Includes Asset Backed Securities (‘ABS’), Mortgage Backed secu rities (‘MBS’), Commercial Mortgage Backed securities (‘CMBS’), Collatera lised Debt Obligations (‘CDO’), Collateralised Loan Obligations (‘CLO’), Col lateralised Mortgage Obligations (‘CMO’).

Primary axis: Amount of collateralised securities in EUR million, Solvency II QRT template S.02.01 row R0170 column C0010

Secondary axis: SCR ratio, Solvency II QRT template S.23.01 row R0620 column C0010

Notes: Solvency II figures, based available data on Solvency II Wire Data — 6 February 2018. Further information available here.