LCP’s eighth annual survey of Solvency II reports from 100 of the largest non-life insurers in the UK and Ireland, published this week, points to the ongoing strength of the insurance market and highlights the increase of emerging risk reporting in the SFCRs.

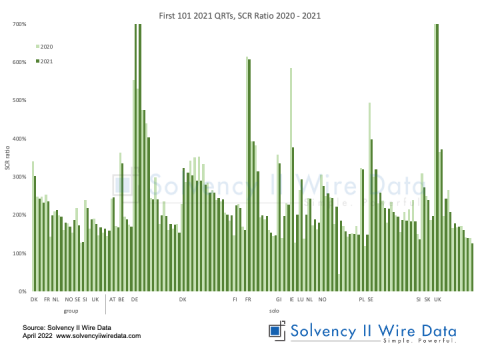

UK and Irish non-life market solvency ratio

The aggregate solvency ratio of the sample (also called the Eligible Own Funds ratio) continued its year-on-year rise to 198% in 2023.

This year’s survey also includes a calculation of the mean solvency ratio, which is less influenced by extreme values; and which has also increased, to 191%.

Growing narrative reporting in the SFCRs

Over the years the surveys have increasingly expanded on text analysis of the SFCRs.

Katie Garner, senior consultant, LCP, co-author of the report, told Solvency II Wire that there has been a steady shift over the years towards providing more clear and comprehensive narrative information in the SFCRs, especially around risk management and governance.

“We are pleased that we have seen a growing trend towards more tailored, company-specific disclosure, rather than being boilerplate. Environmental, social, and governance (ESG) considerations in particular are pushing firms to improve their narrative disclosures to address broader risk factors.”

Rising emerging risks

This year’s report features a dedicated section on emerging risks, which were mentioned by 83 insurers in the sample.

It also includes a list of emerging risks detailed in the SFCRs, by type. These include: Societal, Operational and strategic, Environmental, and Technology risk.

A risk radar published in the HCC International SFCR is spotlighted as an example of best practice.

However, the report also notes some of the limitations in the SFCRs. “Far fewer firms provide details on their current emerging risk processes or how these risks are communicated with senior stakeholder.”

Commenting on the overall quality of the narrative reporting in the SFCRs, Ms Garner added: “One of the major gaps is the lack of consistency in how insurers describe their approach to risk, particularly around emerging risks like climate change and cyber risk. Some insurers still provide vague or high-level descriptions without enough detail on how these risks are being measured and managed.

Providing more detailed insight into the scenarios considered, the rationale behind them, and their real-world implications would enhance the usefulness of these reports for multiple stakeholders, including regulators and investors.”

Further SFCR text analysis

Other sections of the report dedicated to analysis of the SFCR texts include: Cyber and AI risk, Climate change, and Pandemic risk.

A section on Regulation and reporting includes IFRS 17, the reforms to Solvency II and the introduction of Solvency UK.

A forward-looking approach needed

Speaking more broadly on the usefulness of the SFCR documents, Ms Garner argues they could benefit from additional focus on future outlooks.

“SFCRs often focus on historical performance and existing risks, but they could benefit from more forward-looking assessments. Insurers generally provide little detail on how they are preparing for future risks or evolving market conditions.”

The full report: Balancing risk and opportunity in an uncertain world is available on the LCP website.

Download the report here: Balancing risk and opportunity in an uncertain world

Related Articles