Sponsor’s Feature

EIOPA’s final Guidelines for the preparation of Solvency II look set to require firms and supervisors to put in place elements of the new regime by 1 January 2014. In this report William Coatsworth, Consulting Actuary and John McKenzie, Principal and Consulting Actuary, at Milliman take a detailed look at the guidelines, note what has changed after the consultation and comment on the practical implications for firms.

1. Introduction

On 27 September 2013, the European Insurance and Occupational Pensions Authority (EIOPA) published its final guidelines for the preparation of Solvency II. These set out ![]() EIOPA’s proposal for the phased introduction of specific aspects of the Solvency II requirements into national supervision from 1 January 2014, in advance of the full implementation of the Solvency II regime with the aim of ensuring that “National Competent Authorities (NCAs), insurance companies and groups take active steps towards implementing certain key elements of Solvency II in a consistent and convergent way”.

EIOPA’s proposal for the phased introduction of specific aspects of the Solvency II requirements into national supervision from 1 January 2014, in advance of the full implementation of the Solvency II regime with the aim of ensuring that “National Competent Authorities (NCAs), insurance companies and groups take active steps towards implementing certain key elements of Solvency II in a consistent and convergent way”.

The final guidelines and accompanying explanatory text take on board many of the comments received during the consultation period, run from 27 March 2013, covering:

- System of governance

- Forward looking assessment of the undertaking’s own risk (based on Own Risk and Solvency Assessment (ORSA) principles)

- Submission of information to NCAs

- Pre-application for internal models (IMs)

1. Intro 2. Overview 3. CP08 SOG 4. CP10 Reporting 5. CP09 FLAOR 6. CP11 IMAP 7. Summary

2. Overview of the final guidelines

EIOPA notes that generally, responses to the consultation of the guidelines supported a move towards a harmonised regime and welcomed a consistent approach to the preparation of Solvency II across jurisdictions.

While EIOPA has stressed that these guidelines are intended to help firms and supervisors prepare for Solvency II (rather than an early introduction of the regime), it highlights that in order for this preparation to be meaningful, “defined and demonstrable” progress towards Solvency II needs to be made. The final guidelines include clarification that while NCAs are expected to ensure firms meet the outcomes specified in the guidelines, failure by firms to comply with the Solvency II Pillar I requirements during the preparatory phase should not trigger supervisory action.

NCAs have to report to EIOPA within 2 months from the publication of these preparatory guidelines whether they comply or intend to comply with each guideline. In the event that NCAs do not comply with a guideline they need to provide the reasons for non-compliance.

Proportionate and principles-based approach

In response to stakeholder comments, EIOPA has emphasised that the application of the guidelines by NCAs should be proportionate to the “nature, scale and complexity inherent in the business of the insurance and reinsurance undertaking”.

In order to support this application, EIOPA notes that the guidelines are largely “principle-based or drafted with a view to the outcome and supervisory objective that should be met”.

Timings for the preparatory phase

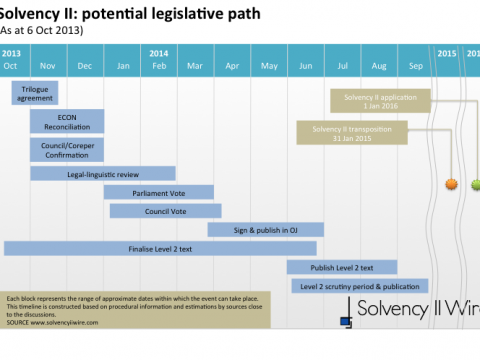

EIOPA has commented that the guidelines have been drafted based on the assumption that Solvency II will be applicable from 1 January 2016.

The timelines set out in the final guidelines largely depend on the finalisation of the Omnibus II Directive. While discussions on this text have been on-going since the beginning of 2011, recent developments indicate that these may be concluded by the end of 2013 in time for final approval at the European Parliament plenary session on 3 February 2014. Official publication of the Omnibus II Directive is expected 2 months after the plenary vote.

We note that these timings appear to be backed up by the draft Directive put forward by the European Commission on 2 October 2013 formally postponing the application date of the Solvency II Directive to 1 January 2016.

EIOPA has further assumed that the final Solvency II Directive (comprising of the Omnibus II text and accompanying delegated acts) will be available in time for NCAs and firms to prepare for the submission of the forward looking assessment during 2014 and 2015 and the quantitative and qualitative reporting information in 2015.

Once the Solvency II Directive has been made available, EIOPA will prepare technical specifications covering the Pillar I quantitative issues, including the valuation of technical provisions, valuation of assets and liabilities other than technical provisions, the calculation of the Solvency Capital Requirements (SCR) and guidance on the assumptions underlying the standard formula calculation.

While the dates proposed in the guidelines will be reviewed at the end of 2013 based on the latest developments with regard to Omnibus II, EIOPA has commented that any delay in the Solvency II process would not impact the need to perform a FLAOR from 2014 onwards on a best effort basis.

Application to third countries

One key concern raised by stakeholders during the consultation period was the application of the guidelines to firms in countries outside of the EEA. In response to this, EIOPA has clarified that it does not expect supervisory authorities in third countries to apply the preparatory guidelines and that the guidelines are only intended to apply to EEA-based groups (and specifically not to apply to EAA branches of third country-based groups).

Where EEA groups have subsidiaries in third countries, they are permitted to use the solvency capital requirements and eligible own funds based on local regulations, effectively assuming that all third countries are considered equivalent during the preparatory phase.

EIOPA has commented that the guidelines are aimed at ensuring that both NCAs and firms progress in their Solvency II preparedness during the preparatory phase. Through implementing these, NCAs should ensure that firms take active steps towards implementing the relevant parts of the Solvency II framework.

As such, the emphasis is put on NCAs to determine how best to incorporate these preparatory guidelines into their regulatory or supervisory frameworks and what powers and tools to use at a national level.

While EIOPA has specified that no supervisory action should result from these guidelines in relation to the Solvency II Pillar I requirements, firms would be expected to ensure the information arising from the implementation of the System of Governance or from the Forward Looking Assessment of Own Risks are considered in the performance of the business or future business planning. Furthermore, where information is provided on the calculation of the SCR and determination of Own Funds, EIOPA has commented that NCAs are expected to review the quality of this information and may take supervisory action if this raises concerns.

3. Final guidelines on the system of governance

Where implemented, the final guidelines on the System of Governance will require all firms and groups falling under the Solvency II Directive to take appropriate steps to build:

- An effective System of Governance

- An effective Risk Management System with strategies, processes and reporting procedures necessary to identify, measure, monitor, manage and report, on a continuous basis and at an individual and at an aggregated level, the risks to which they are or could be exposed, and their interdependencies

- Qualitative information supporting the System of Governance.

System of Governance

Under the proposed guidelines, NCAs are required to ensure that:

- The administrative, management or supervisory body (“AMSB”) (whether at solo or group level) is engaged with the management process.

- The organisational structure established by the AMSB maintains an adequate segregation of duties, is proactive and challenging, supports the strategic objectives and operations of the firm and is capable of being adapted if these objectives change.

EIOPA has commented that guideline 6, which requires any significant decisions of the firm to involve at least two persons who effectively run the firms before the decision is implemented, was almost universally criticised during the consultation period – although it notes that stakeholders have different concerns. In response to these concerns, EIOPA has clarified that “persons who effectively run the undertaking” are not limited to the AMSB but may include senior management members.

The explanatory text provides examples of significant decisions that should fall under guideline 6, specifying that these should not include day-to-day decisions but are rather decisions that are unusual or that will, or could, have a material impact on the firm.The key functions of risk, actuarial, internal audit and compliance are established and are operationally independent (with the exception of internal audit which must be fully independent).

- The scope and frequency of internal reviews of the System of Governance are established, with the scope, findings and conclusions of the reviews documented and reported to the AMSB.

- The firm has contingency plans addressing areas where it considers itself to be vulnerable which are reviewed, updated and tested on a regular basis.

The guidelines further specify that significant decisions that could, or will, have a material impact on the firm must be made by at least two persons who effectively run the firm, and that any decisions made by the AMSB are documented. Policies must also be documented to establish their purpose, the process by which they are applied, the accountability for processes and reporting, and the obligation for the organisation to inform the key functions of relevant facts.

Risk Management System

The guidelines specify that NCAs should ensure that the AMSB is responsible for the effectiveness of the risk management system, setting risk appetite and risk tolerance limits, and approving the risk management strategies and policies. The guidelines set out the requirements for these elements of the risk management system, including the items to be covered in a risk management policy, and the need for the risk management function to report information to the AMSB, both on risks that have been identified as potentially material and on other specific areas of risk either on its own initiative or as requested by the AMSB. Particular features of underwriting and reserving risk, operational risk, asset-liability management, investment risk and liquidity risk are highlighted, as are the requirements for maintaining a policy for risk mitigation techniques.

The accompanying explanatory text expands on these guidelines, requiring firms to consider explicitly strategic and reputational risks as part of their risk management procedures, including the “interconnectedness between these risks and other material risks”, highlighting the potential impact these risks may have on the business. These risks should be included in the risk management policy where relevant.

Own Funds Requirements

The proposed guidelines require NCAs to ensure that firms are developing a capital management policy which includes procedures to ensure the Own Funds items satisfy (at issue and subsequently) the applicable capital regime. The policy should include controls on issuance and set out the approach to managing dividends and distributions.

The development of a medium-term capital management plan is also in the scope of the guidelines. The plan should include consideration of the output from both the risk management systems and the forward looking assessment of the undertaking’s own risks (based on the ORSA principles).

Internal Controls

NCAs should ensure that firms are promoting internal controls by making all personnel aware of their roles in the internal control system and ensuring that there is an appropriate reporting process within this system to support decision making. Where applicable, NCAs should ensure the internal control systems are applied consistently across groups.

Group-Specific Governance Guidelines

The final guidelines require NCAs to ensure groups have appropriate governance arrangements in place to steer risk management and internal control at an individual level. This should have regard to the reporting requirements, and the tools and processes needed to identify, measure, monitor and control risks, taking into account the interests of all entities and how these contribute to the common purpose of the group.

The guidelines address the group-specific challenges of contagion risk, interdependencies between risks from conducting business through different entities and in different jurisdictions, third country entities and from regulated and unregulated companies.

Further guidelines extend the scope of risk management and IM specification to a group context.

The final guidelines on the System of Governance are broadly consistent with those set out in the consultation paper published by EIOPA in March 2013 and with the requirements of the draft Solvency II Directive. However, there are a number of areas of clarification within the accompanying text aimed at addressing the specific concerns of stakeholders.

Specific concerns were raised in relation to a number of the guidelines including:

• Fit and proper requirements

• The roles and responsibilities of the key functions, including the compliance, actuarial and internal audit functions

• Risk management, in particular the content of the risk management policy

• The setting of operational risk limits

• Inclusion of the prudent person principle

• Governance of Own Funds

• Outsourcing

For the majority of these, EIOPA has commented that the guidelines do not go beyond what is set out in the Solvency II Directive and, as such, has not modified its recommendations. While EIOPA acknowledges some of the extra burden these requirements will have on firms during the preparatory phase, it has retained the guidance, emphasising that firms will need to have processes and procedures in place to address these items by the start of Solvency II.

4. Final guidelines on the submission of information to NCAs

The final guidelines set out EIOPA’s proposal for the information that firms will need to submit to NCAs during the preparatory phase. This includes both quantitative and narrative reporting (although only a subset of the full narrative reporting requirements expected under Solvency II will be required during the preparatory phase).

Under the final guidelines, firms will still need to submit one set of annual reporting information before the applicable date of Solvency II, and quarterly reporting for one quarter before this date (rather than two quarters as set out in the earlier proposal). Based on the current implementation assumptions, firms will need to submit annual information as at 31 December 2014 and quarterly information in respect of 30 September 2015.

We note that firms falling within the specified reporting thresholds should be notified of this by their NCA 11 months before the initial submission reference date. Based on the current implementation assumptions, firms required to provide reporting information to NCAs should be informed of this requirement no later than 31 January 2014.

EIOPA has acknowledged concerns around parallel running of Solvency I and Solvency II based systems during the preparatory phase but has commented that this is an unavoidable consequence of moving between regimes. While we expect the two week extension of the annual reporting deadline will be welcomed by firms, this will only go some way to reducing the burden on firms over the year end reporting period.

While no annual submission of information is required in respect of the final year of the preparatory phase, we note that article 302bis of the draft Level 2 requirements looks likely to require all firms to submit an opening Solvency II balance sheet as at 31 December 2015 together with details of the SCR and Minimum Capital Requirement (MCR). While the level of granularity required for these items is unclear at this stage, we note that this should be accompanied by a qualitative explanation of the differences between the value of the assets and liabilities relative to Solvency I, potentially requiring a degree of parallel reporting to continue once Solvency II is in force.

The submission deadlines for annual information have been increased such that individual firms will need to submit annual reporting information 22 weeks after the reporting year end (28 weeks for groups) while quarterly information will still be required within 8 weeks of the quarter end.

EIOPA notes that while the information provided may rely on estimates and simplified methods, the extent to which these can be used will be greater for quarterly submissions than for the annual reporting. Where approximations are used, firms will need to ensure that the information provided is reliable and complies with the relevant Solvency II standards.

Significantly, firms currently applying for the use of a full or partial IM under Solvency II will still be required to submit information on the SCR calculated under the standard formula. However, this will now be submitted as part of the information required under the guidelines on pre-application of IMs, rather than as part of the information submitted to NCAs, and hence not subject to the annual and quarterly reporting deadlines.

While firms will be required to submit quantitative and qualitative information in electronic form, EIOPA has left it up to each NCA to decide on whether this should be done using the XBRL taxonomy proposed for use under Solvency II.

Threshold for reporting

Firms representing at least 80% of the national market share will be required to submit annual quantitative and narrative information to NCAs, while firms representing 50% of national market share will also be required to submit quarterly information. Groups with more than EUR 12 billion of total assets as at the reporting period ending 2012 will be required to provide both quarterly and annual information.

Quantitative information to be provided

The information required to be submitted annually by those solo entities falling within the annual reporting threshold includes:

- Content of the submission (new form)

- Basic information

- Balance sheet

- Assets and liabilities split by currency

- Detailed list of assets and derivatives

- Technical provisions

- Own Funds

- Solvency Capital Requirement (SCR)

- Breakdown of the components of the SCR

- Minimum Capital Requirement (MCR)

The items above highlighted in bold are required to be submitted as part of the quarterly quantitative information for firms falling within the quarterly reporting threshold.

In addition to the above, groups are required to submit annual information covering:

- Entities in the scope of the group

- Insurance and reinsurance solo requirements

- Other regulated and non-regulated financial entities including insurance holding companies solo requirements

- Contribution to group technical provisions

The quantitative templates to be used for the preparatory phase have been renamed to reflect the final approach proposed to be used under Solvency II. A mapping table for the new template names is provided in Appendix IV to the guidelines.

Updated quantitative reporting templates (QRTs) and LOG files have been included as an Appendix to the guidelines incorporating number of changes, together with a comprehensive change log setting out details and explanations of the changes.

While many of these changes have been made in order to correct for errors/mistakes, there are a number of more significant changes to the reporting requirements including:

- Cells regarding information on Ring-Fenced Funds (RFFs) and any simplifications used have been included in a number of templates

- The templates for reporting the SCR calculated using the standard formula or partial IM have been modified to better reflect the relationship between the elements of risk modules calculated using standard formula and a partial IM

- The templates for reporting the SCR calculated using a full IM have been modified to include information on the approaches used to calculate the loss absorbing capacity of technical provisions and of deferred taxes

Narrative information to be provided

The guidelines propose that the narrative report to be provided during the preparatory phase should include information on the following areas:

- General governance requirements – including the system of governance, fit and proper requirements, risk management system, internal control system and governance structure

- Capital management – including information on Own Funds, and explanation of any material differences between the equity shown in the financial statements and the excess of assets over liabilities as calculated for solvency purposes

- Valuation for solvency purposes – covering information on the valuation of assets, technical provisions and other liabilities

Stakeholders have requested that the information they need to submit during the preparatory phase is aligned with the information requested by the European Central Bank (ECB) for the purposes of market monitoring and financial stability analysis, and to serve the needs of the European Systemic Risk Board. In response to this, EIOPA has noted that it has held discussions with the ECB and that the reporting package proposed for the preparatory phase is sufficient to meet the ECB’s expected initial requirements. Despite this, EIOPA has emphasised that its priority is ensuring the Solvency II reporting requirements (and the sub-set of these required during the preparatory phase) are tailored to the information required for the supervisory review process, rather than aligning these with the ECB requirements.

While EIOPA’s proposal that IM firms should still provide information on the SCR calculated using the standard formula falls short of stakeholders requests. The proposal to include this only as part of the information required for pre-application of IMs (and not as part of the annual and quarterly information submitted to NCAs) should help firms with the added burden this calculation creates. EIOPA has emphasised that where reporting is done using an IM during the preparatory phase, firms need to prepare for the eventuality that their IM may not be approved in time for day-one reporting under Solvency II and establish contingency plans in respect of this.

Reporting of internal model firms

IM firms will be required to submit information on the SCR using both the standard formula and using their full/partial IM.

The information calculated using the IM should be provided under the requirements set out in the guidelines on submission of information to NCAs, while the information calculated using the standard formula is defined under the guidelines on pre-application of IMs.

Reporting of groups

EIOPA has confirmed that where firms within a group fall below the threshold on an individual level, they should still be subject to reporting at a group level where the group as a whole is subject to preparatory reporting.

For the purposes of the preparatory phase, all third countries should be considered as equivalent. The approach for the calculation of group SCR should be determined by the group in discussions with the group supervisor (the consolidation method remains the default approach and any decision not to use this should be justified to the group supervisor).

Reporting of ring-fenced funds (RFFs)

Firms are required to submit information on major material RFFs, based on notional SCR, at both an individual and group level during the preparatory phase. Non- material RFFs are to be reported together with the remaining non-RFF business.

Reporting of (re)insurance captives

For the purposes of the preparatory phase, EIOPA has permitted NCAs to exempt captives from the need to submit quarterly information relating to Q3 of 2015. EIOPA notes that captives would still need to provide annual reporting information and that this exemption should not be taken as an indication of future solutions under Solvency II.

Reporting of third country branches

Third country branches operating in the EU are excluded from the reporting requirements during the preparatory phase.

5. Final guidelines on forward looking assessment

The guidelines require firms falling within the specified thresholds to perform a forward looking assessment covering three main aspects:

- Assessment of overall solvency needs

- Assessment of whether the firm would comply with Solvency II regulatory capital requirements and technical provisions on a continuous basis

- Assessment of deviations from the assumptions underlying the SCR calculation.

Consistent with the Solvency II ORSA requirements, the forward looking assessment should ensure that the firm engages in the process of “assessing all the risks inherent in its business and determining its corresponding capital needs”. This requires firms to have in place adequate and robust processes to assess, monitor and measure their risks and overall solvency needs. Fundamentally, these processes need to be fully embedded within the business as part of the decision-making process of the firm.

The guidelines emphasise that the assessment should be bespoke to the firm and, as such, there is no fixed way specified for structuring this.

EIOPA has clarified that the assessment of overall solvency may be performed on “local recognition and valuation bases (or statutory accounts)” on a best effort basis. However, where a different basis to Solvency II is used, firms should demonstrate that this is a more appropriate approach during the preparatory phase (rather than just being easier).

Thresholds

All firms falling under the Solvency II Directive will be required to perform an assessment of their overall solvency needs starting in 2014.

EIOPA has commented that groups applying for a (partial) IM are not expected to perform the assessment of the deviation of the risk profile from the assumptions underlying the SCR calculation. However, it is not clear whether solo firms in the IM pre-application process would be similarly exempt. Guideline 16 permits firms to perform a qualitative analysis as a first step which may provide such firms with a quick way of demonstrating that a further quantitative assessment is not required.

In addition, firms representing at least 80% of the national market share, and groups with more than EUR 12 billion of total assets as at the reporting period ending 2012, will be required to perform an assessment of compliance on a continuous basis with Solvency II regulatory capital requirements and technical provisions starting in 2015.

Timings for the FLAOR

Under the final guidelines, firms are expected to perform the assessment of their overall solvency needs at least two times during the preparatory phase, once in 2014 and once in 2015, regardless of any changes to the Solvency II implementation timeline. EIOPA has confirmed that the first assessment of overall solvency needs is expected to be performed at any time during the year 2014.

EIOPA will prepare technical specifications in 2014 covering Pillar I technical issues and guidance on the assumptions underlying the standard formula. As such, the assessment of continuous compliance with regulatory capital requirements and technical provisions together with the assessment of any deviations from the assumptions underlying the SCR calculation will not be required until 2015. The need for firms to quantitatively estimate the impact of different recognition and valuation basis for the assessment of overall solvency will similarly not be required until 2015. As the technical specifications depend on the finalisation of the Omnibus II Directive, these dates will be reviewed at the end of 2013.

We note that the timings for the preparation and submission of the FLAOR have been a cause of confusion for many firms since the draft guidelines were first published in March 2013 and we welcome the clarification of these by EIOPA. The final guidelines specify that all firms are expected to perform an assessment of their overall solvency needs during 2014. As such, firms should now look to ensure that they have appropriate processes in place to carry this out.

The deferral to 2015 of the requirements to provide continuous assessment of compliance with capital requirements and technical provisions, as well as an assessment of deviations from the assumptions underlying the SCR calculation, should be welcomed by firms, many of which had questioned the ability to perform this effectively while the Solvency II Pillar I requirements were still under discussion.

However, we note that this will mean that firms may only get one attempt to iterate these specific items with NCAs before Solvency II goes live. While this may give firms longer to develop and implement the relevant processes and procedures, they should maintain regular dialogue with supervisors throughout this period to help ensure these areas meet the required outcomes and supervisory objectives.

Use of the FLAOR

During the preparatory phase, firms are expected to ensure that the results and insights from the forward looking assessment are used throughout the business, and at least in the following areas:

- Capital management

- Business planning

- Product development and design

The explanatory text details that any strategic or other major decisions that may materially affect the risk or own funds’ position of the firm need to be considered in the context of the forward looking assessment before such a decision is taken.

In order to achieve this, the AMSB should ensure it has an active role in the FLAOR such that it can steer the assessment and challenge the results. EIOPA has stressed that it “is not acceptable that the AMSB delegates the full responsibility for the forward looking assessment to committees of the AMSB or to senior management, the risk function or another special committee”.

FLAOR for internal model firms

Solo and group IM firms are permitted to perform the FLAOR based on their IM.

However, EIOPA has commented that such firms should also consider the regulatory capital requirements and capital planning implications under the standard formula as well as establishing a contingency plan for non approval of the IM.

FLAOR for groups

As a minimum, all entities that are within the scope of group supervision should be captured within the group FLAOR (although others can be included if appropriate at the discretion of the group). This includes non-EEA entities even if these are not required to perform a FLAOR at an individual level.

The group FLAOR should be performed according to the requirements set out by the NCA of the parent firm.

EIOPA has emphasised that the AMSBs of the individual firms within the group are responsible for their individual FLAORs. Where a single FLAOR is produced covering both the group and the underlying individual firms, the AMSBs of the individual firms must provide assurance that their risks are properly represented. Furthermore, the interrelations and responsibilities between the individual and group AMSBs should be clearly defined.

Where application is being made for a group (partial) IM, the group is not expected to provide an assessment of the deviation of the risk profile for the assumptions underlying the SCR. However, where individual firms within the group continue to us the standard formula to calculate the SCR, such an assessment should still be made at an entity level.

FLAOR for EAA branches

EEA branches of third country (re)insurers are not required to perform a FLAOR.

Documentation of the FLAOR

Firms must maintain the following documentation for the forward looking assessment:

- Policy for the forward looking assessment

- Record of each forward looking assessment

- An internal report on each assessment

- A supervisory report of the assessment.

The final guidelines comment that while it is necessary for firms to develop a full policy for the forward looking assessment during the preparatory phase, this may be part of the policy on risk management. If this is the case the parts or chapters on FLAOR need to be clearly identifiable.

The content of the documentation for the assessment is fully in line with the Solvency II ORSA requirements. The supervisory report should be submitted to NCAs by firms within two weeks of AMSB sign-off of the results of the assessment.

During the consultation period, many stakeholders questioned the need to provide full documentation of the FLAOR in advance of the start of Solvency II. EIOPA has reiterated the need to establish all specified items of documentation, highlighting their importance during the preparatory phase.

We note that while these requirements will inevitably place an additional burden on firms, the preparatory period should allow firms time to develop their documentation in advance of Solvency II. In particular, EIOPA has commented that it anticipates the supervisory report will be developed during the preparatory phase before firms settle on an appropriate form of the report.

6. Final guidelines on internal model pre‑applications

The internal model (IM) pre-application process enables firms to submit their IM applications to NCAs for feedback on their preparedness for final submission. Participation in the pre-application process is voluntary, and participation does not guarantee approval of the formal application.

The final guidelines on IM pre applications take a slightly different approach to the other sets of guidelines. While the other three sets of guidelines provide guidance to NCAs on how to phase-in selected elements of the Solvency II framework, the IM guidelines address an integral part of the process that firms who are looking to have an approved IM in place for day one use under Solvency II must follow.

We note that such firms will most likely be well advanced in their development of an IM, and in demonstrating compliance with the various tests and standards that this must meet, based on draft Level 3 papers published by EIOPA in 2010 and 2011. As such, the final guidelines are broadly consistent with both this previous guidance and the requirements set out in the Solvency II Directive.

The final guidelines expand on these existing requirements, providing more explanation as to what EIOPA expects NCAs to look for during the pre application period and, by implication, in maintaining an IM under Solvency II. Our summary of these has focused on this additional guidance and, as such, should be read in conjunction with the previous draft Level 3 papers to provide a complete overview of the pre-application requirements.

The guidelines outline the aspects of IMs that NCAs must form opinions on during the pre-application process, including:

- Model changes

- Use test

- Assumption setting and expert judgement

- Methodological consistency

- Probability distribution forecast (PDF)

- Calibration – approximations

- Profit and loss (P&L) attribution

- Validation

- Documentation

- External models and data

- Functioning of colleges

Model changes

IM firms must establish a written model change policy, outlining the procedures in place to ensure the IM meets the Solvency II requirements on an on-going basis.

The explanatory text states that a model change policy should cover the following aspects:

- The sources of change

- The identification of a need for change

- The classification of changes as major or minor

- The governance of changes

- The reporting of changes

The guidelines clarify that the policy is not intended to cover extensions of the model scope, such as the inclusion of additional risks or business units, nor changes to the policy itself. Such changes should be classified as ‘major’ and hence automatically subject to supervisory approval. However, EIOPA has confirmed that updating of parameters can fall within the scope of the model change policy, as they can have a significant impact of the model outputs, and the SCR in particular.

Where IMs contain a large number of interrelated parameters, EIOPA suggests that it may be more appropriate for firms to consider and describe the impact of changes to such parameters in batch rather than individually. Where this is done, the policy should also explain why this approach is appropriate and detail the circumstances under which this would cease to be the case.

A key criterion used to classify model changes as major or minor will be the impact of the change on the SCR. The Guidelines state that the prevailing market conditions can be taken into account when judging the impact of a model change on the SCR. EIOPA also suggests that a firm can leverage any internal classification of model changes in order to classify changes as major or minor using a clear mapping between the classifications.

Assumption setting and expert judgement

The final guidelines contains guidance on what NCAs should look for during the pre-application process with regards to assumption setting and expert judgement within the IM, including the communication, documentation and validation of assumptions.

The guidelines state that firms should:

- Obtain AMSB sign-off for the most material assumptions

- Document the materiality of each assumption and also the rationale of the expert judgement behind each assumption

- Obtain an independent review (internal or external) of the assumptions as part of the validation process.

The explanatory text clarifies that where firms use quantitative indicators and metrics to assess the materiality of assumptions, these should consider both individual and aggregate materiality. Proportionality should be applied when documenting assumptions. As such, it may not be necessary to provide extensive documentation on all cases where an assumption is based on expert judgement.

Probability distribution forecast (PDF)

Previous guidance has required firms to have processes in place which aim to ‘increase’ knowledge of their risk profile, including knowledge of the risk drivers and other factors explaining the behaviour of the variable underlying their PDF. The final guidelines relax this requirement such that a firm is now only required to “maintain sufficient and current knowledge of its risk profile”.

NCAs should take into account the following when assessing the ‘richness’ of a firm’s PDF:

- Whether the PDF reflects the firm’s risk profile

- The current progress in actuarial science and generally accepted market practice

- Any measures that the firm puts in place to ensure compliance with IM tests and standards

- For each risk, the way in which the techniques chosen, and the resulting PDF, interact with the richness of the PDFs of other risks

- The nature, scale, and complexity of the risk.

EIOPA clarifies that firms should not simply adopt market practice without some adaptation for their specific risk profiles. Similarly, NCAs should not urge firms to adopt market practice but should simply use market practice as a reference point when assessing firms’ approaches.

Profit and Loss Attribution

The P&L is previously defined as the change in basic Own Funds not attributable to capital movements. The guidelines acknowledge that the IM may use other monetary amounts to determine the change in basic own funds such as economic capital resources.

Throughout the pre-application process, NCAs must form a view on how firms ensure the relevance and adequacy of the P&L attribution process. Firms will be expected to regularly evaluate and document (at least annually) how the results of the P&L attribution might be used within their risk management and decision making framework.

The explanatory text states that NCAs must gain comfort that firms ensure:

- The P&L attribution includes all material risks and not just those modelled internally

- The attribution methods remain sufficiently consistent over time to allow a useful comparison of the P&L attribution from one period to another.

Validation policy

The final guidelines provide more explicit guidance on what EIOPA expects to see in validation policies, including details on:

- The processes, methods and tools used to validate the IM and their purpose

- The frequency of regular validation for each part of the IM and the circumstances that trigger additional validation

- The persons who are responsible for each validation task

- The procedure in the event that the validation process identifies problems with the reliability of the IM and the decision-making process to address those concerns.

The explanatory text states that validation policies may differentiate between types of validations, e.g. initial, implementation, and on-going validation. For each type of validation, the policy may state:

- The topics (e.g. data quality, expert judgement) covered by the specific type of validation

- The type and volume of activities (e.g. desk research, interviews, tests) performed

- Some criteria or threshold to specify when the validation is passed or failed.

Firms should consider the materiality of the part of the IM being validated both in isolation and in combination with the rest of the model. Where individual parts of the model are not validated accurately due to their lack of materiality, NCAs must ensure that firms have considered that those parts may be material when taken in combination.

In relation to the governance surrounding the validation process, EIOPA now explicitly states that, where the results of the process need to be escalated, the escalation path should be defined in such a way as to maintain the independence of the validation process.

Group internal models

The group specificities of the use test have been expanded from the draft Level 3 text.

The guidelines require NCAs to be comfortable that all firms within a group who will use the group IM are cooperating to ensure the design of the model is aligned with their businesses and risk management systems. This includes ensuring the outputs are granular enough to allow the group IM to play a sufficient role in each firm’s decision making process.

Individual firms must provide evidence that:

• The individual SCRs will be calculated at least once a year, and more frequently if the firm’s risk profile changes significantly, and whenever needed as part of the decision making process

• It is able to propose changes to the group IM for components that are material to them or following a change in their risk profile or in local conditions

• It possesses an adequate understanding of those parts of the IM which cover risks related to their business, for example by having access to up-to-date and relevant model documentation

Validation policy for group internal models

EIOPA states that a single validation policy should be established to cover the validation process at both group and solo entity level

Functioning of colleges

The guidelines address the practicalities of the pre-approval process for cross-border groups, as well as the areas that colleges should consider when forming a view about the appropriateness of the scope of a group IM:

• The significance of firms within the group with respect to the risk profile of the group

• The risk profile of firms within the group compared to the overall group risk profile

• Any transitional plan to extend the scope of the model at a later stage

• The appropriateness of the standard formula or alternative IM used to calculate the SCR of a firm within the scope of the group IM

Validation process

The risk management function retains overall responsibility for model validation and is expected to ensure the validation process is independent from the development and operation of the model. When deciding the parties which will contribute towards the validation process, EIOPA requires firms to take into account the nature, scale and complexity of the risks the firm faces, the function and skills of the people to be involved and the firm’s internal organisation and governance system.

The explanatory text clarifies that the validation process can leverage activities performed by non-independent parties but these cannot be relied on entirely. The most material tests, calculations and analysis must be performed by people not involved in the development of the IM.

‘Good practice’ for the risk management function with respect to validation of modelling performed by external parties includes:

- Staying in close touch with the external party and consider any appropriate follow-up

- Assessing the activities performed by the external party to ensure they are free from restrictions and limitations that might influence the outcome

- Ensuring that a realistic budget and timeframe are put in place for the services to be performed

- Ensuring that there is no conflict of interest between the external party and the person performing the validation activities.

Documentation

Building on existing guidance, the guidelines state that documentation of circumstances under which the IM does not work effectively should cover:

- The risks not covered

- The limitations in risk modelling

- The nature, degree and sources of uncertainty of results, including the sensitivity of the results

- The deficiencies in data

- The limitations of information technology

- The limitations of governance.

EIOPA also clarifies that where firms are required to document their plans for model improvements, such plans should be at a high-level and a detailed model development plan is not required.

External Models and Data

In validating external models, the guidelines state that firms should assess the appropriateness of the selection, or otherwise, of features or options which are available for the external models.

EIOPA clarifies that it is the firm’s responsibility to provide specific information to NCAs about any external models used to allow them to make the requisite assessments. NCAs should reject applications for using external models if this requirement is not met.

7. Summary

The final guidelines for the preparation of Solvency II set out EIOPA’s proposal for the phased introduction of specific aspects of the Solvency II requirements into national supervision from 1 January 2014, with the aim of ensuring a consistent and convergent implementation of the following items:

- System of governance

- Forward looking assessment of the undertaking’s own risk (based on Own Risk and Solvency Assessment (ORSA) principles)

- Submission of information to NCAs

- Pre-application for internal models (IMs)

Throughout the final guidelines EIOPA has sought to emphasise that while these will place extra burdens on firms, this is balanced by the benefits that this will bring in preparing firms for the outcomes that will be required under Solvency II.

Under the proposed guidelines, all firms will be required to implement a System of Governance in line with Solvency II requirements and submit an assessment of overall solvency needs from 1 January 2014.

In addition, firms identified by NCAs as falling within the specified thresholds will be required to submit annual and quarterly information as at 31 December 2014 and 30 September 2015 respectively. In 2015, these firms will also be required to perform an assessment of whether they would comply with Solvency II regulatory capital requirements and technical provisions on a continuous basis as well as an assessment of deviations from the assumptions underlying SCR calculation. These items will be based upon technical specifications that EIOPA intends to issue during 2014.

EIOPA has commented that the timings of the preparatory phase are based on the assumption that Solvency II will be applicable from 1 January 2016. This will largely depend on the finalisation of the Omnibus II Directive and, as such, EIOPA has committed to revisit this at the end of 2013.

—

Views expressed are the authors’ own.