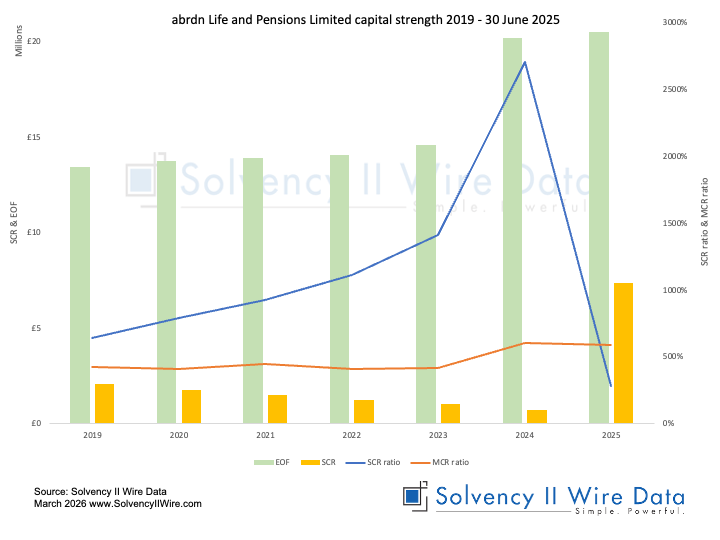

abrdn Life and Pensions Limited published an interim SFCR reflecting changes following the Part VII transfer acquisition of Phoenix Life Limited, which was completed in March 2025.

The SFCR published as at 30 June 2025 shows that the acquisition resulted in a massive decrease in the firm’s solvency ratio, down from 2,736% in December 2024 to 279% in June 2025.

The driver for the drop is the increase in SCR from GBP 0.74 million to GBP 7.35 million, while the eligible own fund remained relatively unchanged at GBP 20.48 million.

The increase in eligible own funds is explained in the SFCR as follows:

“The total own funds have increased since 31 December 2024. This primarily reflects the increase in the net of tax contribution to own funds from the excess of the VIF over the risk margin (£3.53m) and profits over the six months to 30 June 2025 (£1.57m), offset by the … [part VII] transfer acquisition payment of £4.00m”

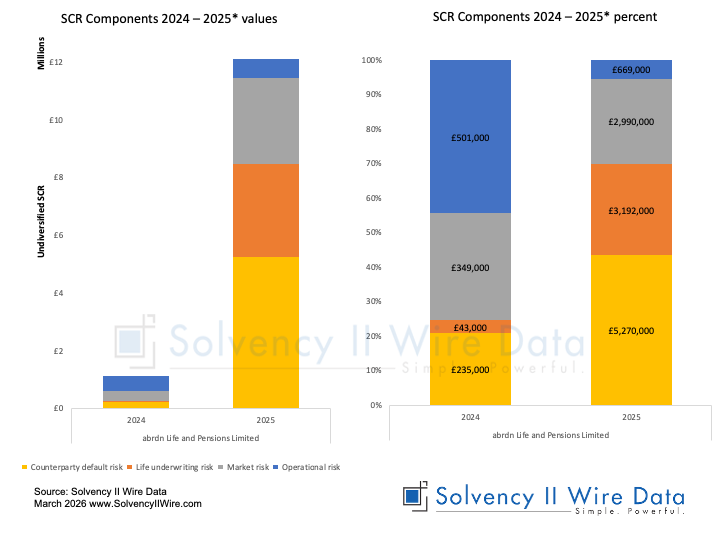

The change in the SCR is driven by three major factors described in the report:

- An increase in the counterparty default risk capital requirement, primarily reflecting the introduction of unit-linked investment only reinsurance ceded to Phoenix Life.

- An increase in the life underwriting risk capital requirement, primarily reflecting the increase in the VIF following the … transfer, where the proportion of that increased VIF lost under the lapse stress contributes to the capital requirement.

- An increase in market risk, again primarily reflecting the increase in the VIF following the Arbour transfer and the loss of a proportion of the increased VIF under the market stresses applied to linked assets.

SCR components swings and roundabouts

The total undiversified SCR of the firm increased from GBP 1.7 million to GBP 12.78 million over the reporting period.

The components of the SCR – market risk, life underwriting risk, counterparty default risk and operational and other risk – are detailed in the new template IR.25.04.01 under the UK Solvency regime.

All increased significantly due to the aquisition (see charts below).

However, their proportion of the SCR changed. Both counterparty default risk and underwriting risk ballooned, while the proportion of operational risk, (which increased by the smallest amount) shrunk from almost 50% of the SCR to less than 10%.

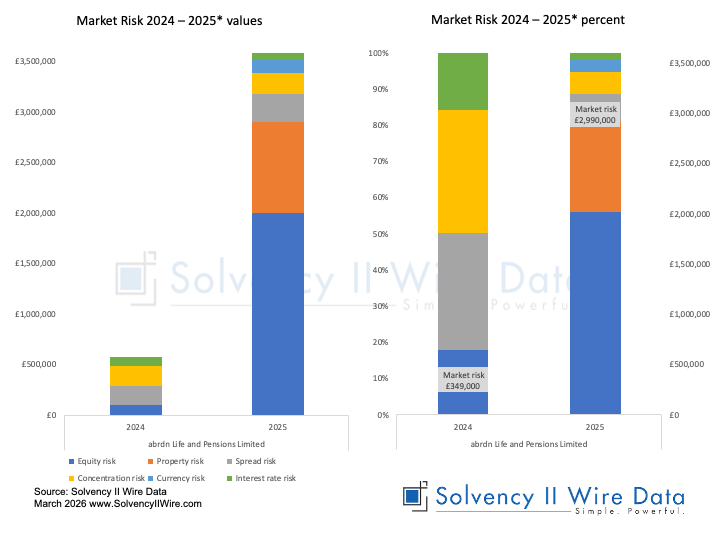

Market Risk

Similarly, the make-up of the firm’s market risk profile also changed.

Spread risk and concentration risk, which jointly accounted for almost 70% in 2024 (see charts below) are now dwarfed by equity risk, and property risk. The latter was introduced with the acquisition of Phoenix Life Limited.

It is expected that abrdn Life and Pensions Limited will produce a full 2025 SFCR (as at 31 December 2025) in April.