Reporting of market risk sensitivities in the SFCR is rising up the regulatory agenda, as can be evidenced in the recent EIOPA publication on the Solvency II 2020 Review.

In its June 2019 consultation on the Solvency II 2020 Review, in a section entitled ‘Gaps identified in the SFCR information’, EIOPA explains the underlying motivation for enhancing risk sensitivity disclosures. “The information on the risk sensitivity to different scenarios or stresses, should be better structured and more comprehensive”.

The consultation also calls for greater comparability in the way market sensitivities are disclosed by insurers in the SFCR. “The information regarding the SCR and risk sensitivity is not comparable across different undertakings/groups. It is expected that the reporting of sensitivities to different scenarios or stresses is disclosed in a more structured format.”

The call for greater comparability in the Solvency II disclosures will be welcome by industry. Both analysts and asset managers have made several proposals for standardisation of the data in public and private. It appears that EIOPA has taken such views into consideration when laying out a proposed standard for market sensitivity disclosure in the consultation document.

“Based on the best practices of the market EIOPA proposes to require the disclosure of information on the impact on the SCR coverage ratio and impact on the amount of the Own Funds in million euros of the following key sensitivity tests.” The initial proposal, although somewhat reduced in its final version, suggests disclosure of both economic and non-economic assumptions.

Economic assumptions

- – Equity markets (-25%)

- – Equity markets (+25%)

- – Interest rates (-50bps)

- – Interest rates (+50bps)

- – Credit spreads of government bonds (-50bps)

- – Credit spreads of government bonds (+50bps)

- – Credit spreads of corporate bonds (-50bps)

- – Credit spreads of corporate bonds (+50bps)

- – Real estate values (-25%)

- – Real estate values (+25%)

Non-economic assumptions

- – 10% increase in expenses

- – 10% increase in gross loss ratio

- – 10% increase in lapse rates

Disclosing market risk sensitivities in the SFCR

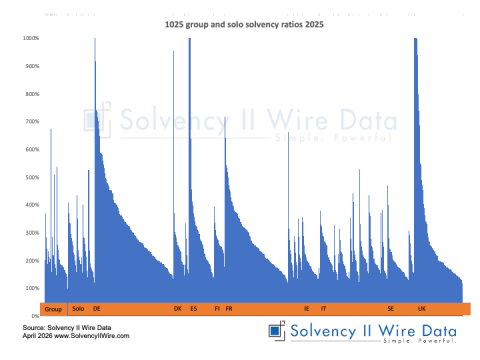

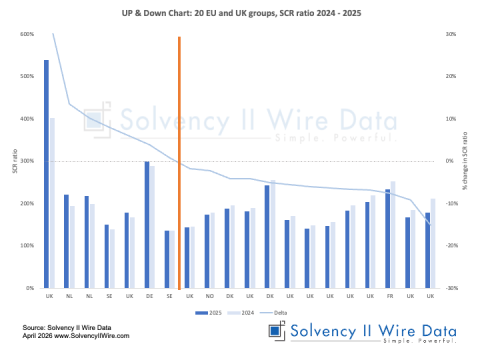

The extent to which such standardisation can be reached may be observed by reviewing the market sensitivities disclosure in the SFCRs for year-end 2019.

Analysis conducted by Solvency II Wire Data of the SFCRs of 100 European groups (including the 50 largest groups by total assets) reveals that just over 50 percent of SFCRs contained market sensitivity data.

Around a quarter of the sample also published an additional breakdown of the SCR components.

By far the most common stresses tested are government and corporate spread risk, equity risk and interest rate risk. Standardisation remains somewhat of an issue given the wide range of stresses and impacts that are being reported.

—

Find out more about market sensitivity data available to premium subscribers of Solvency II Wire Data service here.

Solvency II Wire Data collects all available public QRT templates for group and solo.

QRT templates available on Solvency II Wire Data

S.02.01 Balance sheet

S.05.01 Premiums, claims and expenses Life & Non-life

S.05.02 Premiums, claims and expenses by country Life & Non-Life

S.12.01 Life and Health SLT Technical Provisions

S.17.01 Non-life Technical Provisions

S.19.01 Non-life Insurance Claims Information

S.22.01 Impact of long term guarantees and transitional measures

S.23.01 Own funds

S.25.01 SCR Standard formula

S.25.02 SCR Standard Formula Partial Intern Models

S.25.03 SCR Standard Formula Intern Model

S.32.01 Undertakings in the scope of the group