Publication of the Solvency II 2019 SFCRs and QRTs has gotten off to a slow start. By close of business on the reporting deadline (7 April) only about 300 of the 3,330+ Solvency II firms had published their reports.

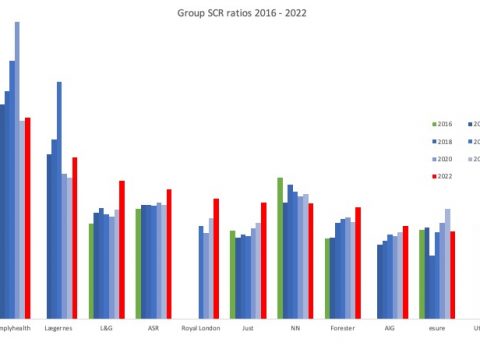

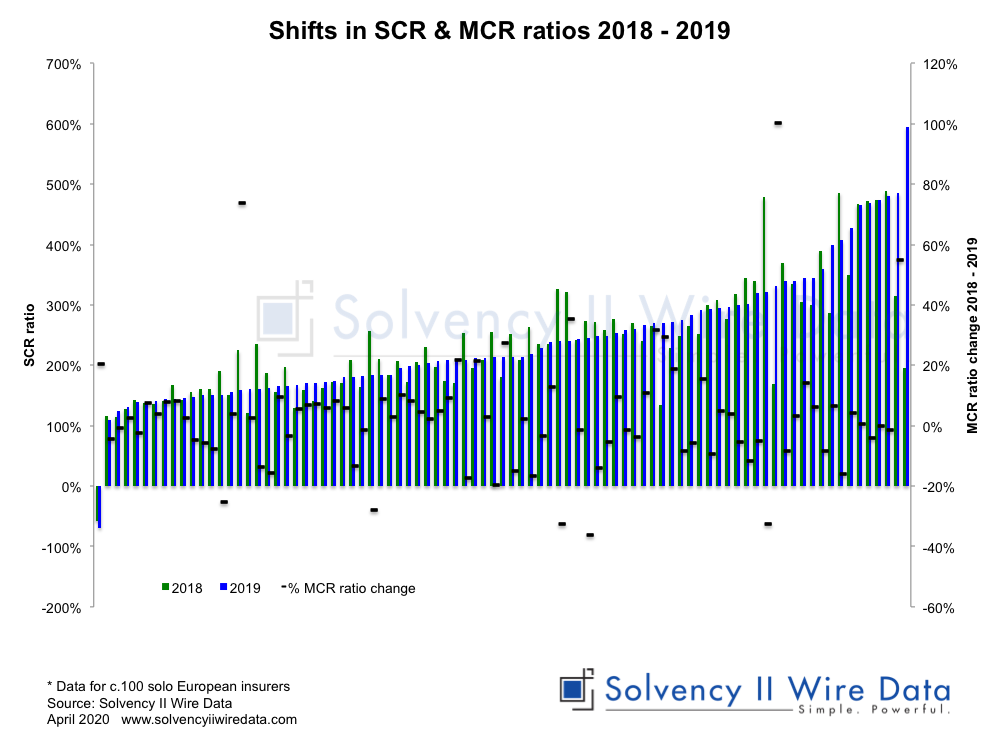

Analysis of the first 2019 QRTs conducted by Solvency II Wire Data shows that SCR ratios have remained relatively constant.

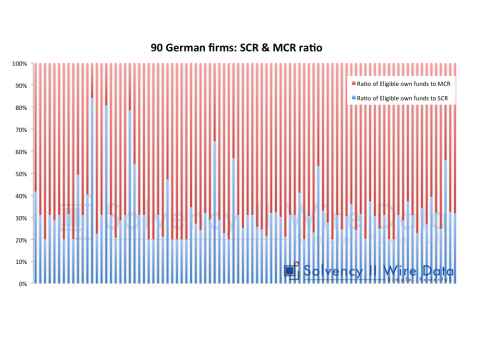

The chart below compares the SCR ratios of c.100 solo insurers between 2018 and 2019 (bars, left axis) plotted against the change in the MCR ratio for the same period (line, right axis).

Overnight a number of the larger groups published group and solo figures as well.

On 20 March 2020 EIOPA published recommendations for a set of delayed reporting options to help insurers manage during the corona virus crisis. The majority of firms have so far published the full set of QRTs and SFCR including the COVID-19 note as requested by EIOPA. For early analysis of the COVID Note see here.

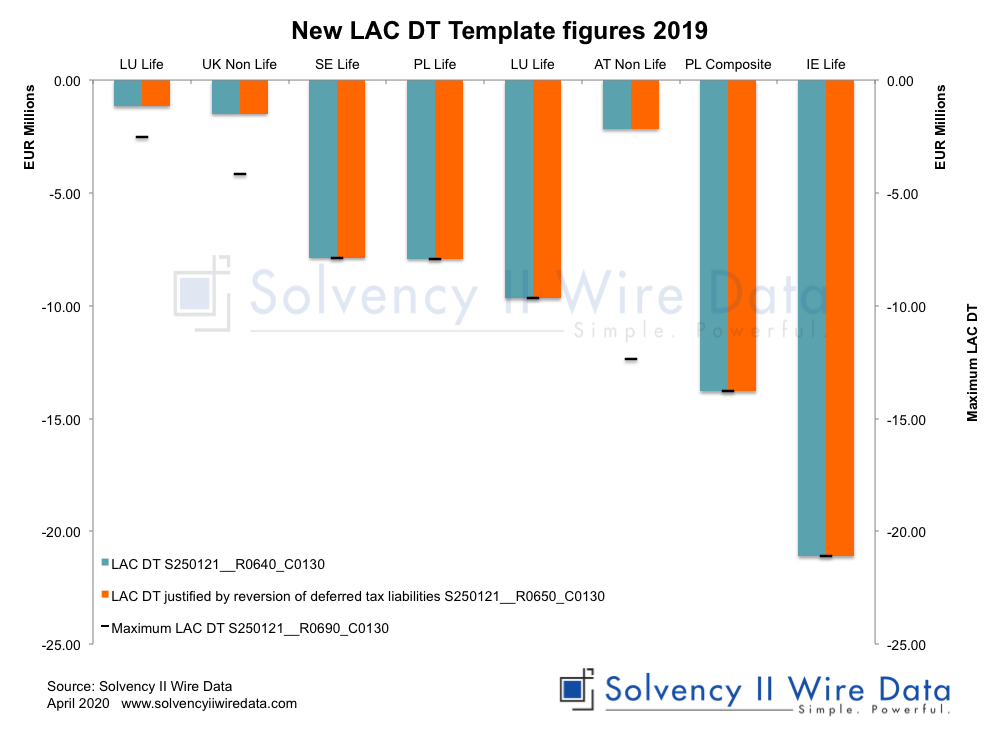

Additional LAC DT cells in S.25

This year sees the publication of the first of the new fields included in template S.25 to reflect more information on the way the Loss Absorbing Capacity of Deferred Taxes (LAC DT) is calculated.

Details of the changes were published on 27 November 2019 (see COMMISSION IMPLEMENTING REGULATION (EU) 2019/2102). Data for these cells is now available on Solvency II Wire Data.

So far 8 insurers published the new templates. The chart below compares LAC DT (S250121__R0640_C0130) and LAC DT justified by reversion of deferred tax liabilities (S250121__R0650_C0130) relative to the Maximum LAC DT (S250121__R0690_C0130, lines, right axis)

COMMISSION IMPLEMENTING REGULATION (EU) 2019/2102 of 27 November 2019 explanation fields

The Commission Implementing Regulation defines the fields as follows:

LAC DT

Amount of loss-absorbing capacity of deferred taxes, as defined in Article 207 of Delegated Regulation (EU) 2015/35.

LAC DT justified by reversion of deferred tax liabilities

Amount of loss-absorbing capacity of deferred taxes, calculated in accordance with Article 207 of Delegated Regulation (EU) 2015/35 justified by reversion of deferred tax liabilities.

Maximum LAC DT

Maximal amount of LAC DT that could be available, before the assessment whether the increase in net deferred tax assets can be used for the purposes of the adjustment, as provided for in Article 207(2) of Delegated Regulation (EU) 2015/35.

Solvency II reporting and COVID-19

Over the coming days it will become more clear exactly how many firms will use the full scope of the delay allowed by EIOPA, although the early indications are that, much like the rest of the economy, COVID-19 is affecting the insurance sector and the Solvency II universe.

Solvency II Wire Data collects all available public QRT templates for group and solo.

QRT templates available on Solvency II Wire Data

S.02.01 Balance sheet

S.05.01 Premiums, claims and expenses Life & Non-life

S.05.02 Premiums, claims and expenses by country Life & Non-Life

S.12.01 Life and Health SLT Technical Provisions

S.17.01 Non-life Technical Provisions

S.19.01 Non-life Insurance Claims Information

S.22.01 Impact of long term guarantees and transitional measures

S.23.01 Own funds

S.25.01 SCR Standard formula

S.25.02 SCR Standard Formula Partial Intern Models

S.25.03 SCR Standard Formula Intern Model

S.32.01 Undertakings in the scope of the group