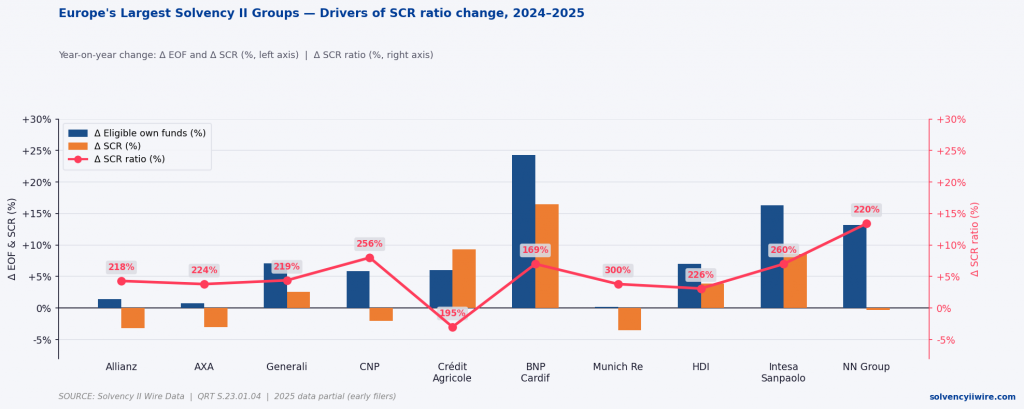

Nine of the ten largest Solvency II insurance groups recorded a higher SCR ratio in 2025 than in 2024, according to Solvency II Wire Data.

Across the sample as a whole, aggregate eligible own funds (EOF) rose by 5% to EUR 405.6bn while aggregate solvency capital requirement (SCR) grew by just 1% to EUR 178.2bn, lifting the aggregate SCR ratio from 218% to 228% — a gain of 4%.

Ratio Movements

The majority of groups recorded ratio increases in the range of 3% to 8%, with two outliers — NN Group and Crédit Agricole Assurances — at the extremes.

- Allianz Group moved from 209% to 218%, a year-on-year change of +4.3%.

- AXA Group rose from 216% to 224%, a change of +3.8%.

- Assicurazioni Generali S.p.A. — Generali Group rose from 210% to 219%, a change of +4.4%.

- Groupe CNP Assurances recorded the second-largest gain in the set, rising from 237% to 256%, a change of +8.0%.

- Crédit Agricole Assurances was the only group to record a decline, falling from 201% to 195%, a change of -3.0%.

- BNP Paribas Cardif Group rose from 158% to 169%, a change of +7.0%; it remains the lowest-ratio firm in the set.

- Munich Re crossed the 300% threshold, moving from 289% to 300%, a change of +3.8%.

- HDI Group moved from 219% to 226%, a change of +3.1%.

- Gruppo Intesa Sanpaolo Assicurazioni rose from 243% to 260%, a change of +7.0%.

- NN Group N.V. recorded the largest year-on-year movement in the set, rising from 194% to 220%, a change of +13.4%.

* Data for Groupe Prudentiel UNMI was not available at the time of publishing.