The Solvency Margin Ratio (SMR) is the measure of insurance capital adequacy strength in Japan. The metric, which will soon be replaced by the more market-consistent and Solvency II-like Economic Solvency Ratio (ESR) is reported by all insurers on an annual basis; and many of the larger firms report quarterly as well (see for example Tokio Marine).

The SMR is calculated by dividing the available capital (called the solvency margin) by half the amount of the required capital (risk amount). The Japanese Financial Services Agency (JFSA) details the components and calculation of the SMR.

Data collected by the Japan Insurance Database provides insights into the distribution of the SMR among Japan’s solo insurers.

The analysis includes 60% of non life solo insurers and over 50% of life insurers and is based on reporting for the financial year 2024, ending on 30 March 2025.

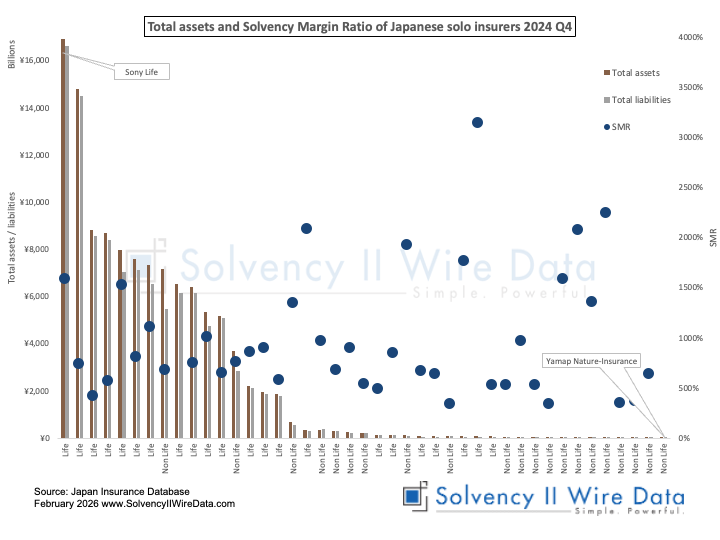

The chart below shows the distribution of companies ranked by total assets.

The largest company in the sample is Sony Life Insurance Company, which reported JPY 16.9 trillion of total assets in its general accounts. The smallest is Yamap Nature-Insurance reporting JPY 732 million.

The distribution of ratios seems uncorrelated with the size of the balance sheet, however it is notable that the bulk of the larger firms are life insurers.

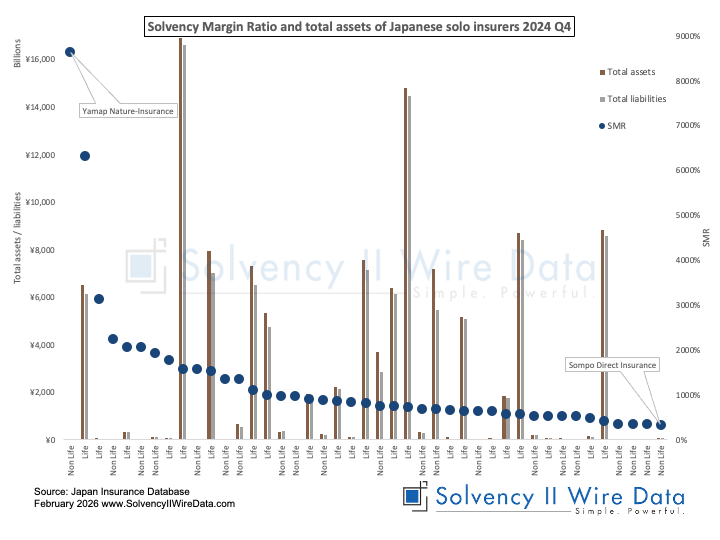

Arranging the data by SMR (see chart below) confirms the lack of correlation between the SMR and balance sheet size.

Yamap Nature-Insurance reported the highest Solvency Margin Ratio 8,654.9%. The lowest SMR, 342.3%, was reported by Sompo Direct Insurance, which is one of the ten largest companies in the sample.

What is notable is the more even distribution of life and non life insurers across the full spectrum of ratios in the sample.

The Japan Insurance Database is powered by Solvency II Wire Data.