The Solvency II Wire Quarterly is a general update on the state of Solvency II implementation as reflected in the Solvency II Wire Regular Meeting Groups (RMGs) and other Solvency II Wire activity.

The RMG brings together a wide range of practitioners to discuss Solvency II and related matters. The following is a summary of the key discussion topics addressed at the meeting.

In this issue

1. Solvency II Barometer

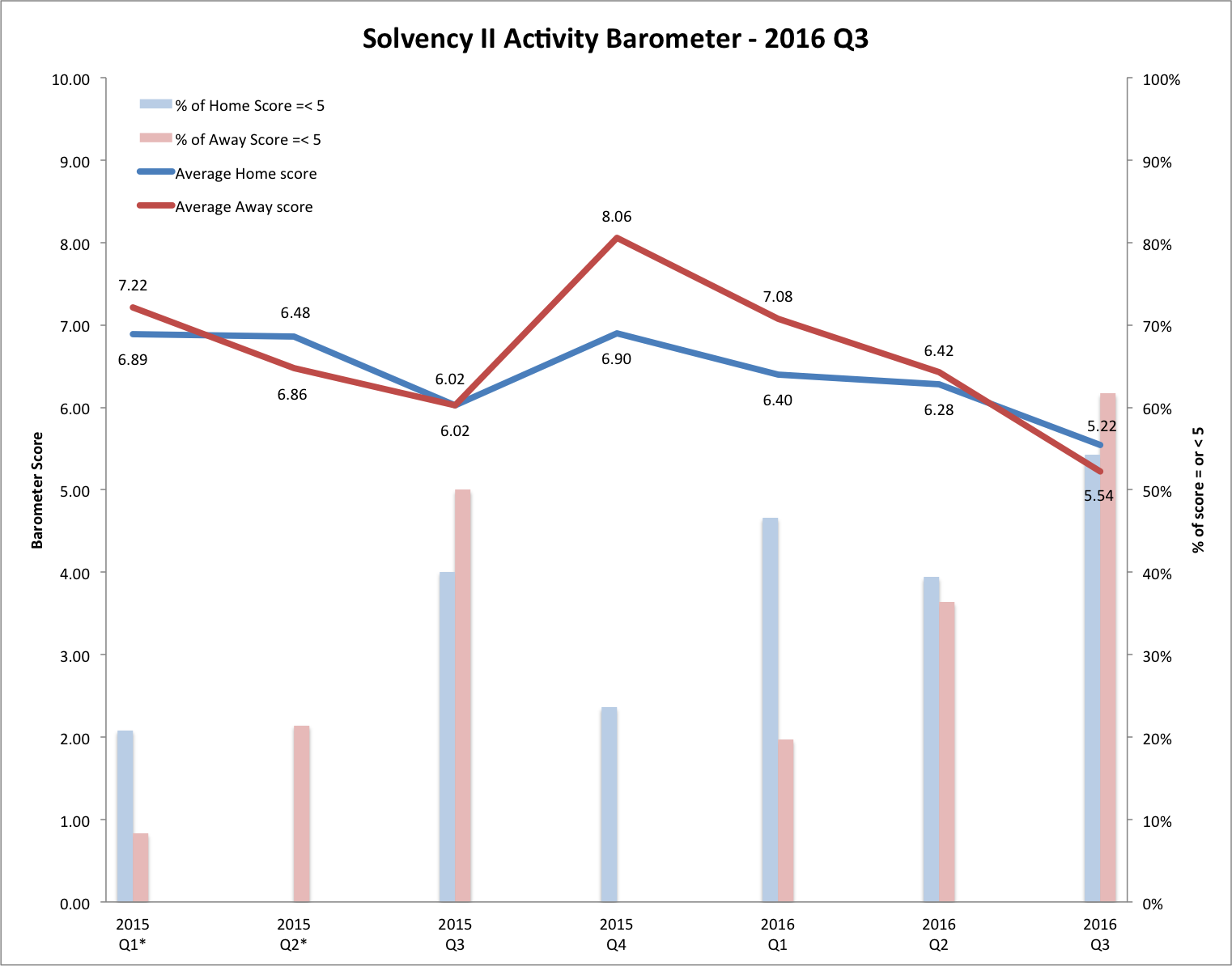

For the past year participants in the Solvency II Wire Regular Meeting Groups (RMGs) have been asked to rank the level of Solvency II activity in their own work (Home score) and that of their organisation or the market, as they see it (Away score). The score is on a scale of 1-10, where 10 represents 100% of the time spent on Solvency II.

The chart shows a clear downward trend in Solvency II activity since the start of the year. The figures strongly correlate with the rise in scores equal to or lower than 5 over the period.

The results are most likely a product of a shift to business as usual (BAU), especially following the Day 1 and the first quarterly reporting submissions, and the need to focus on matters beyond compliance including Brexit, product design and porfolio optimisation.

We expect an uptick in the fourth quarter as firms prepare for annual reporting and public disclosures.

2. Report

The RMGs in the third quarter focused on reviewing some of the emerging impacts of Solvency II and Brexit. It is now clear that Solvency II can no longer be viewed in isolation. The interaction between the two and the low-yield environment are the strongest indication yet that Solvency II is becoming another component of BAU.

Solvency II: so much or not much?

Reflecting on the impact of Solvency II since the Directive entered into force in January, many commented that it was somewhat underwhelming.

As one participant noted in the review meeting in August, most of the work had already been done in the run-up to implementation and the transition into BAU had already started before the end of the year.

However, in areas such as reporting, it is increasingly looking like getting to BAU will be an on-going process. Although the first two reporting exercises of the year passed with little incident (see Quarterly 2016 Q2) – it emerged that in several cases NCAs did not apply all the validation criteria when accepting the data – most information transfers progressed smoothly.

Asset managers continue to report difficulty in delivering asset data, mostly at a more nuanced level, for example, granularity and materiality for look-through reporting.

Public disclosures: the stampeding elephant on the horizon

Pillar III will continue to play an important part of Solvency II work as attention turns to the public disclosures in 2017.

Some firms indicated that they required the QRTs to be approved at board level, while others said they have obtained CFO signoff only after initial consultation with the board. Participants from both large and small insurers acknowledged that the public disclosures would require board level approval.

Overall the operational cost of compliance was becoming apparent as insurers are beginning to understand the impact of extensive regulatory reporting programs on their resources and costs of operation.

The good stuff in Solvency II

The first six months of Solvency II have also begun to show some of the benefits of the new regime.

Firms are starting to gain greater awareness or formalisation of thought processes about required capital levels, solvency and risks generally. These were leading to an industry-wide change in both the levels of capital and a more cautious, risk-averse approach to investment. However, as described in further detail below, there is increasing pressure to invest in riskier assets in the quest for yield.

Insurers using an Internal Model are also beginning to understand their real risk exposure at a much more granular level as well as the areas of profitability within the business.

Brexit – loss of passporting horrors

Without a doubt the question of passporting is at the forefront of the industry’s Brexit concerns.

Loss of direct access to the single market would make it more difficult for firms to operate in Europe. A number of participants expressed concern that the likely consequences of this would be to constrain the growth potential of UK insurers in Europe.

What’s more, many third countries rely on the UK to passport business into the EU. One of the main benefits for the UK has been substantial inflow of Foreign Direct Investment, which could dry up if passporting rights are lost.

The viability of relocation or setting up a branch in an EU country was likely to depend on the amount of business the firm did in Europe as well as the specific country where the business was concentrated. The latter may prove critical in the choice of location.

Relocation also raises questions about outsourcing requirements under Solvency II, which are likely to be observed quite closely by national regulators. In addition, it remains to be seen if they would accept a “name plaque” relocation or require significant set up of staff and resources.

Meanwhile, France has made an open play to attract UK insurers and other financial services firms by announcing a fast-track and simplified licensing procedures for UK based firms operating in France using the passporting mechanism.

Less UK influence on Solvency II

Whatever (or if any) Brexit deal is finally negotiated it is certain that UK insurers would, in effect, still be subject to Solvency II; either via direct regulation or some form of equivalence. One concern for the industry will be the UK’s diminishing influence on any future changes to the rules. It is unlikely to win such lucrative carve-outs as the Matching Adjustment in future.

A further concern for the insurance industry is that its priorities will be secondary to those of banking, asset management and clearing that have traditionally held more sway with policy makers.

Surprise review of UK insurance regulation

Several participants at the meeting expressed surprise at the announcement of the UK Parliament’s Treasury Select Committee review of EU insurance regulation.

Few in the industry have an appetite to rewrite Solvency II and it is likely that the outcome of the consultation will be pressure on modifying some of the more contentious aspects of Solvency II such as:

- Risk Margin sensitivity to interest rates,

- treatment of dynamic Volatility Adjustment,

- treatment of Equity Release Mortgages and other illiquid assets,

- quantitative Indicator framework,

- nature of internal model approval and change process,

- nature of Matching Adjustment approval and change process,

- ‘Model drift’ monitoring,

- look-through requirements, and

- external audit requirements for SFCR

There is an unavoidable sense that the review may have been, at least partially, politically motivated in the current Euro-bashing, post-Brexit referendum environment.

On 30 April 2013, Andrew Tyrie MP, the Committee’s much respected chairman, chose to publish an exchange of letters with the PRA criticising Solvency II and notoriously branding Solvency II as: “an object lesson in how not to make law”. The publication was made less than two days before the UK national local elections, when the anti-European factions of the ruling Conservative party were putting pressure on then-prime minister David Cameron.

Solvency II is also one of the few financial services regulations that the UK can openly attack, given its European origins, as opposed to regulation such as CRD IV, which originate with the international Basel Committee on Banking. And as the UK prepares to compensate for any trade loss with Europe by turning to international trade it would make no sense to be criticizing these rules.

Equivalence again

If the UK leaves without access to the single market it would probably have to apply for, or gain, Solvency II equivalence. And while it could comfortably argue that it would automatically be compliant, given the full implementation of the directive in the UK today, it is worth considering that equivalence is generally granted on the basis that the third country is working towards full equivalence, which in the case of the UK will be moving in the opposite direction.

2 x Solvency II?

Some also floated the idea that the UK adopt a two-tier regulation, one for domestic insurers and another, more closely aligned to Solvency II, for cross-border firms. The difficulty here is the increased complexity that may outweigh any benefit. For example, the UK has a number of very large domestic insurers, Prudential, for example, that have little business in Europe but a substantial presence in the UK and other parts of the world.

Brexit’s toxic legacy

But perhaps one of the more toxic economic impacts of Brexit will be the continuing low interest rate environment (see the BoE’s decision to cut interest rates shortly after the referendum vote) and the weakening exchange rate, which are raising concerns about an inevitable rise in inflation.

There are now also genuine emerging concerns that the impact of the low yield environment is starting to spread beyond the life insurance business to non-life firms that are feeling the strain of a near decade-long low investment returns.

Investing in a Solvency II world

The July RMG looked at the emerging investment strategies and trends in the Solvency II environment.

Quest for yield overshadows capital charges

The impacts of Solvency II were considered by many as secondary to the continuing low yield environment. Insurers continue to try to balance the search for yield through alternative and riskier assets within the constraints of the SCR. There was a strong suggestion that the balance was tipping towards the quest for yield at the expense of optimisation for capital charges.

It was suggested that some institutions are now close to the 50% mark in illiquid fixed income strategies.

Linking products with investment

The current environment was also driving a growing realisation that investment strategy has to be taken into consideration when designing products. It is becoming apparent that the old practice of designing a product and finding a suitable investment portfolio was no longer viable.

Drifting away from government debt

Many are seeing a shift away from government debt towards corporate debt, driven by yield and anticipated regulatory change. For example, in Italy the shift is driven by low and declining sovereign yields, but perhaps also with an eye on the potential introduction of risk charges for sovereign debt in the Solvency II standard formula and EIOPA concerns about sovereign concentration risk.

Further notable trends are an increased focus on hedging currency and inflation risks and de-risking the insurance balance sheet through the use of reinsurance and capital-light strategies.

3. Solvency II Statistics

Much has been made of the volatility of the Solvency II balance sheet. Over the coming years market participants and regulators will be watching these numbers closely. Analysis conducted by Solvency II Wire based on publically disclosed Solvency II figures in the first half of 2016 starts to shed light on the figures and the factors that shape them.

The analysis comprises 28 firms (mostly groups) that reported Solvency II figures on 31 December 2015 and 30 June 2016, in 9 countries.

The Solvency Capital Requirement (SCR) ratios of the sample range between 123% – 263% (170.5% average) at the start of the year and 122% – 252% (167.5% average) at the end of June.

For the majority of firms in the sample the change in SCR ratio over the period was less than +/-10% and is therefore used as the base line for the analysis.

6 firms experienced wider fluctuation over the period. The most notable changes were for experienced by Delta Lloyd 32%, KBC -19% and CNP -14%.

Figure 1. SCR Ratio 31 Dec 2015 – 30 Jun 2016, below shows the SCR ratio variation for each firm (SCR ratio = own funds / SCR). There appears to be little correlation between the size of the ratio and its fluctuation over time. Similarly there is no discernable correlation if the ratio increases or decreases. [gview file=”https://www.solvencyiiwire.com/wp-content/uploads/2016/10/SCR-Ratio-31-Dec-2015-30-Jun-2016.pdf”]

Figure 2. Changes in: SCR ratio, own funds and SCR 31 Dec 15 – 30 Jun 16 compares the percentage change in the SCR ratio (orange line) against the percentage change of the own funds (black line) and the SCR (blue line), for each firm.[gview file=”https://www.solvencyiiwire.com/wp-content/uploads/2016/10/Changes-in-SCR-ratio-own-funds-and-SCR-31-Dec-15-30-Jun-16.pdf”]

The comparison shows some of the factors affecting the change in the SCR ratio. For example, most of Delta Lloyd’s significant increase in the SCR ratio (32%, from 131% to 173%) came from an increase in its own funds (31%) while the SCR was relatively unchanged (-2%, from EUR 3bn to 2.94bn).

In contrast, the 11% increase of Topdanmark’s SCR ratio appears to owe more to a reduction in the SCR (-18%, from DKK4.7bn to 3.86bn).

In some cases a significant change in either own funds or the SCR can result in little change in the SCR ratio. For example, the Swedish insurer Avanza saw a large increase in its own funds (48%, from SEK 2.08bn to 3.07bn), which was accompanied by a similar increase in the SCR charge (57%, from SEK1.24bn to 1.95bn) resulting in a mere 6% decrease in the SCR ratio. A similar pattern can be observed with Rothesay.

The underlying causes of change need to be assessed with caution. Some of the changes to the SCR and own funds were a result of M&A or similar activity. For example, Rothesay acquired a large part of Aegon’s annuity portfolio and Delta Lloyd made some disposals and a €650 million rights issue.

The figures are also still subject to adjustment and restatement. KBC, for example, stated in its 2015 annual report that its SCR ratio at 31 December 2015 was 231%. In the first quarter of 2016 the figure dropped to 201%, however, in its half year report the firm stated that due to an additional capital charge imposed by the Belgian regulator both the first and second quarter figures had to be revised, from 210% to 195% and from 208% to 187% respectively.

To find out more about Solvency II Wire’s data analytics capabilities click here.

The Solvency II Wire Quarterly is a new initiative and we would be very keen to get your feedback on this new initiative. Click here to email the editor directly.

To subscribe to the Solvency II Wire mailing list for free click here.