The Solvency II Wire Quarterly is a general update on the state of Solvency II implementation as reflected in the Solvency II Wire Regular Meeting Groups (RMGs) and other Solvency II Wire activity. The RMG brings together a wide range of practitioners to discuss Solvency II and related matters. The following is a summary of the key discussion topics addressed at the meeting.

In this issue

- Solvency II activity Barometer

- Update

- Readiness surveys

- Predictions for 2016

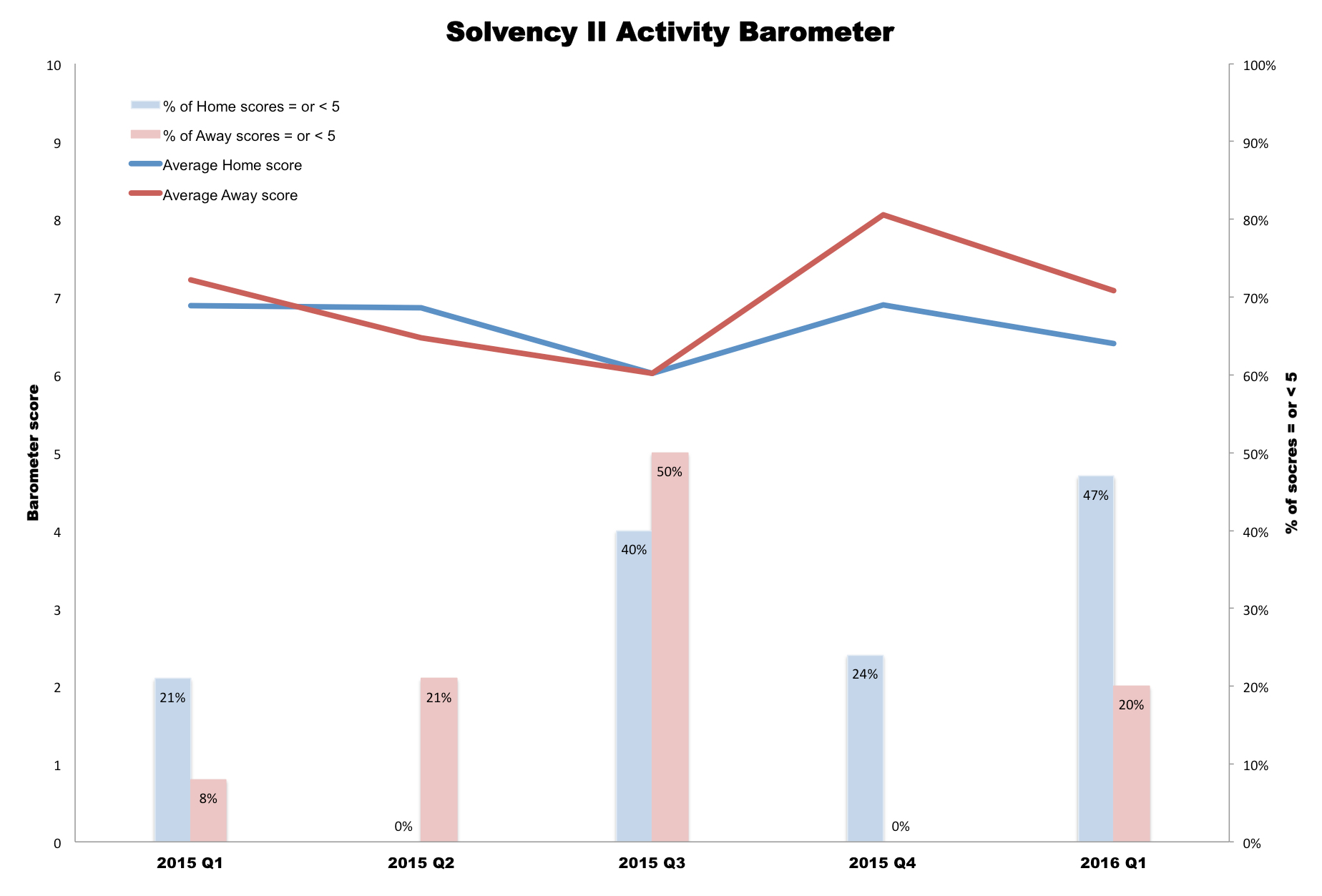

1. Solvency II activity barometer

For the past year participants in the Solvency II Wire Regular Meeting Groups (RMGs) have been asked to rank the level of Solvency II activity in their own work (Home score) and that of their organisation or the market, as they see it (Away score). The score is on a scale of 1-10, where 10 represents 100% of the time spent on Solvency II. The chart shows quarterly figures for three metrics: average home score, average away score and percentage of scores of five or less (Home and Away). The Barometer shows a downward trend in activity through most of 2015, which picked up again in the fourth quarter. Somewhat surprisingly the activity in the first quarter of this year was lower than the previous quarter as well as the first quarter of 2015.

2. Update

The picture of Solvency II implementation to-date is quite patchy and messy and likely to continue to stay this way for some time to come. What appears to be happening is a continuation of the pre entry into force trend that some firms (and markets) have embraced Solvency II, while others continue to drag their feet and treat it as a compliance exercise. The picture is muddied further as those who are advanced in their Solvency II work are encountering new challenges as they progress, for example new reporting requirements for the ORSA forward-looking assessment. Overall activity in the market is increasing as witnessed by the rising number of Solvency II events and Twitter traffic (@solvencyiiwire).

Surprising: number of last minute data requests

Perhaps the most striking revelation at the start of the year, which was made during the January RMG, was the number of asset managers and service providers that reported a substantial increase in Solvency II requests from insurance clients, including several first time requests. Some asset managers also reported that requests were being made late in the quarter only a short time before the day one reporting deadlines.

Unsurprising: Pillar I obsession and reporting still a challenge

Less surprising has been the all too predictable obsession of the mainstream financial press with Pillar I and its impact on M&A. This has been fuelled by the entry into force and increasing numbers of voluntary disclosures of Solvency II figures as part of the first quarter reporting by many insurers. Disclosures will continue to play a major role in the impact of Solvency II well into the next year when the first round of full Solvency II public disclosures begin. What many firms are also realising is the impact of data quality on the reporting speed and that in order to produce the Solvency II reports in the needed frequency high quality, clean data is a must.

Volatility and LTG impacts a concern

Two big questions remain in respect of reporting: understanding the volatility of the numbers over time and the impact of the LTG. For the latter there are signs that some firms are shifting towards semi-annual disclosures although this can hardly be defined as a trend at this point. With regards to the LTG, some anecdotal reports from rating agencies suggest that analysts are looking past the LTG figures to the underlying numbers (without the measures). If this does become the case it is a worrying trend for many insurers in those markets that are so heavily reliant on the measures for their Solvency II figures.

ORSA and SFCR rising

Few firms seem to have given much consideration to their SFCR report, the task is being left for the second half of the year and beyond. But those that have comment on the challenges of publishing the right balance of information. Participants in the RMGs this quarter acknowledged that the SFCR would be a very useful document and would likely become the key document for assessing the condition of firms in years to come. And as firms report over time, close attention will be paid to the variation in numbers and descriptions.

Blurring lines between pillars

As firms move further along the implementation path, they are becoming aware of crossovers between the three pillars. Some have observed the difficulty in separating the ORSA work from Internal Model work as well as improved communication between the actuarial and accounting functions. It is also becoming apparent that some additional internal reporting will be required for Pillar II stress testing and scenario generation.

Rising cost of reporting: rating agencies and look-through

The cost of reporting continues to be a major concern for insures. The two main themes emerging are rating agency fees and look-through reporting. The flag on rating agency charges has been raised by AMICE, the European mutual association. In a press release issued on 29 March 2016 it said that rating agency fees have increased by “up to 80%”, stating: “With the entry into force of Solvency II, credit rating agencies have decided to charge market participants additional costs for the use of the credit rating information in their reporting to NCAs. As a result, insurers have to pay several times for the same information.” AMICE has referred these matters to the various European authorities and is calling for a review of the dependence of Solvency II on credit ratings. The issue was also raised in the January RMG, one participant said they were exploring using alternative rating agencies for the calculation of the Credit Quality Steps (CQS). However, at least one insurance association said it has been engaging with a number of rating agencies for over a year and has come up with pragmatic solutions to the pricing and licensing costs, especially for smaller firms. There is a sense that ultimately this issue will be resolved by the marketplace and it seems like an area crying out for some fintech startup to take up and disrupt. Meanwhile the uncertainty and frustration around the look-though continue. Some reports at the Paris RMG indicate that different controllers were interpreting the proportionality principle differently, with some taking a more pragmatic approach than others. Another view expressed in London is that those firms that tried to provide all the look-through levels found it extremely difficult to do so, while those that took a pragmatic approach and engaged in dialogue with the regulator were able to reach a suitable compromise. Anecdotal evidence about the difficulty of producing advanced layers of look-through abound. At one meeting an example was cited of a portfolio that had 5% of assets held in collective investments and the effort of analysing five levels of look-through for those investments was inverse to its size.

Becoming comfortable with Solvency II

The real impact of Solvency II on the asset allocation and investment strategy of insurers will take a while to assess. But evidence from the meetings suggests it is only one of several factors that will impact investment decisions. The most obvious factor continues to be the low interest rate environment. There are also reports that as firms are becoming more comfortable with the Solvency II balance sheet they are taking another look at optimising their capital position. Although, as reported in the Paris meeting, some believe the emerging work is in the remaining two pillars.

Changes to the rules

As expected, the Commission has made a number of changes to the asset calibrations relating to infrastructure. The guessing games on the review dates of Solvency II continue with some arguing for change as soon as possible, while others call for the rules to be left alone to allow firms to let the system settle in.

3. Readiness survey

Insights from the Thomson Reuters Solvency II Diagnostics tool (disclosure: Solvency II Wire and Thomson Reuters have entered a commercial agreement to share anonymised aggregated data from the tool). The current sample consists of close to 200 insurers, asset managers and providers of data based in Europe, and includes data collected until the end of the first quarter of 2016.

Readiness and ORSA

The data shows that the state of Solvency II readiness has not changed among those insurers surveyed in the first quarter of 2016, with around 70% of the new sample reporting they are ready for Solvency II. However there was an increase of 10% in the number of firms that conducted an ORSA (72%) compared with the pre 2016 sample.

Understanding the EIOPA data requirements

Insurers have displayed a higher level of confidence of understanding the EIOPA data requirements after January. The combined total of respondents that said they were either “somewhat confident” or “very confident” increased to 67% of the sample compared to 63% before January. The number of respondents saying they were “very unsure” they understood the data halved to 7%. For asset managers the picture is reversed. The number of “somewhat confident” and “very confident” responses dropped from 61% to 43%, with most now saying they were “somewhat unsure” (just over 40%).

Sourcing credit rating data and CQS

The Diagnostics Tool also provides insights into the use and sourcing of ratings data. Before January, only 39% of insurers said they implemented a solution to calculate the composite risk rating or Credit Quality Step (CQS) needed for Solvency II. The number dropped to 33% after January. Of those, across the whole sample, 40% are sourcing the data directly from rating agencies, 40% are using asset servicers and a further 20% are using data vendors.

Data audit

About 55 insurers across the sample responded to questions about data audits. Just over half said they had an audit process in place to verify and validate their QRT reports. The percentage of positive responses in the more recent sample was slightly lower than prior to 2016. Only 26% of asset mangers said they were providing their customers with an audit process to verify and validate the Solvency II reports or asset data they were supplying. The percentage of positive responses in the more recent sample was also slightly lower than prior to 2016.

Analysis

The results show no significant change in the level of preparation for Solvency II and a slight increase in ORSA readiness, which is in line with the anecdotal evidence of the continuing trend of uneven implementation. The discrepancy of understanding the EIOPA data between insurers and asset managers might be explained by the fact that after January the number of insurers in the sample dropped by 10%, while it increased by the same amount for asset managers, rather than reflecting a fundamental shift. The findings are at odds with the anecdotal evidence of increase in data requests experienced by asset managers.

4. Predictions for 2016

A selection of predictions from participants at the RMGs on what to look out for this year.

Product and business change

Insurers will continue to work on Solvency II throughout 2016 restructuring their balance sheet and refining their models to optimise Solvency II. There will also likely be an increase focus on risk culture and governance.

Internal models

Most participants expect an increase in the number of Internal Model and Partial Internal Models over the year.

Disclosure and reporting

Increased scrutiny of Solvency II figures will drive a second wave of reporting work. There is a sense that Solvency II reporting is in its infancy and will evolve over time, both for firms and regulators. Some predict EIOPA will publish materiality guidance on look-through reporting.

Market activity

Overall it is expected that M&A activity in the sector will continue as the entry into force of the Directive brings clarity on structure and rules.

Regulation / harmonisation

Many believe that harmonisation will be slow to the point of de-facto uneven playing field across Europe.

The Solvency II Wire Quarterly is a new initiative and we would be very keen to get your feedback on this new initiative. Click here to email the editor directly. To subscribe to the Solvency II Wire mailing list for free click here. [adsanity_group num_ads=1 num_columns=1 group_ids=233 /]]]>