EIOPA is close to finalising the guidelines for the Solvency II interim measures, according to two separate sources involved in the process. The sources, who have seen at least parts of the draft guidelines, spoke to Solvency II Wire in two separate phone interviews. Both reiterated that while the information was based on current draft guidelines it may still be subject to changes.

The current guidelines cover internal models, governance, an ORSA-like process and reporting. Reporting is being formally referred to as “submission of information to national competent authorities,” one source said. A final draft of the guidelines from the EIOPA working groups was circulated to relevant EIOPA members for final comment last week.

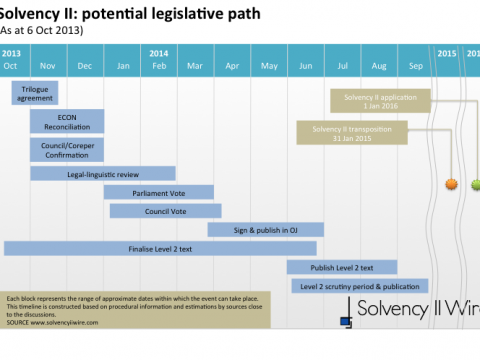

A spokesperson for EIOPA confirmed that the Board of Supervisors (BOS) is planning to review the guidelines at its next scheduled meeting on 26-27 March with a view to launch a public consultation at the beginning of April.

If the public consultation is launched as planned, the sources estimate that the final guidelines will be issued by the fourth quarter of 2013 (following the September meeting of the BOS). Therefore, firms will only know the final version of the full requirements towards the end of 2013. The first interim measures are due to apply as early as the start of 2014.

In December 2012 EIOPA issued an Opinion on Interim Measures Regarding Solvency II, in response to the ongoing delays of the Omnibus II process and concerns that national supervisors were formulating independent strategies to handle the uncertainty and escalating costs. The move by EIOPA aims to provide, “A consistent and convergent approach with respect to the preparation of Solvency II,” the document stated. To that effect, “EIOPA will publish guidelines addressed to national competent authorities on how to proceed in the interim phase leading up to Solvency II.”

It is now understood that a broad consensus has been reached on most parts of the draft guidelines, although it remains to be seen how lack of clarity on capital requirements (currently subject to the long-term guarantee impact assessment) will affect the governance and, in particular, the reporting measures.

The sources noted that Pillar II has been the area over which there have been fewest differences of opinion from national supervisors and industry. However, questions also remain about how the measures will work given the uncertainty around Pillar I and Pillar III.

Despite some pushback from industry, most stakeholders were persuaded that reporting should be included in the interim measures. Both sources confirmed that the guidelines include a number of core templates for annual reporting. There is also an expectation that some quarterly reporting will be included but as yet no final agreement on their extent or timing, one of the sources said.

The reporting templates likely to be included are those relating to information only, e.g. assets, exposure measures or accounting data. Templates that include calculation of provisions, especially for long-term business would be more difficult to produce.

Reporting will be subject to minimum thresholds set by EIOPA, but it is expected that National Supervisors will be able to add firms at their discretion. Consideration is also being given to financial stability reporting and expected ECB reporting requirements. The latter may result in additional information requirements.