Part one: the zero percent capital charge challenge Turmoil in the European government debt markets is calling into question the zero percent capital charge on European government bonds under Solvency II.

This two part article explores how firms and regulators are handling the discrepancy between the charge and real default risk, and what life without a risk-free rate might look like.

Part one examines the implication of a zero percent capital charge on risk-free assets that are anything but. The Solvency II standard formula capital charges aim to help make sure that insurance firms will be able to match their liabilities at a confidence level of 99.5% over a one year horizon.

The charges for a number of asset classes are being contested by the industry but none are more controversial than the 0% capital charge on EEA sovereign bonds issued in their own currency. Let us be clear – what this implies is that these bonds are effectively risk-free and that all countries in the EEA are equally immune to the risk of default.

Clearly a proposition few, if any, would accept today. “Should we rethink the concept of zero risk? I think so,” Gabriel Bernardino, Chairman of EIOPA said at the organisation’s first annual conference in Frankfurt in November. Quite what that ‘rethink’ means is unclear. For now, firms need to move forward with Solvency II preparations. While those planning to use an internal model are likely to factor exposure to sovereign risk in their portfolio already, for firms using the standard formula the solution is as clear as mud.

Putting market panic in perspective

But first some perspective. While European sovereign debt markets are as stable as a wedding cake on the hind quarters of a bull in a rodeo, it does not imply these economies are on the verge of default. “At the moment the market price does not reflect the underlying economic fundamentals for many of the European government bonds,” Dan Morris, Market Strategist at J.P. Morgan Asset Management, said. “Right now these markets are experiencing a buyer’s strike, which is driven more by anxiety and regulatory pressures than by economic fundamentals. In some cases this pressure is driven by clients forcing asset managers to offload their positions.”

Mr Morris noted that the fundamentals of similarly rated sovereigns and debt-to-GDP ratios would suggest the cost of borrowing for Italy and Spain, for example, is too high and it is unlikely that either will default. “However,” he added, “at some point illiquidity can turn into a solvency problem if it persists for long enough.”

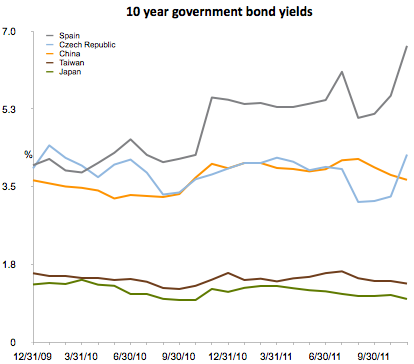

Looking at the chart for 10 year government bond yields for Spain against other similarly rated countries (S&P rating of AA-) shows its borrowing costs are significantly higher. “Of course you can always argue that Spain’s rating should be lowered but they are not currently on negative watch,” he said.

Even though it is unclear when, or how, the European debt crisis will be resolved, insurance firms need to be prepared to handle the current discrepancy between the zero percent capital charge and real default risks that they are exposed to.

Solvency II asset management

An insurance firm’s assets, like those of other investors, are managed against a benchmark. Asset managers will try to match or beat the benchmark according to parameters and needs set by their clients. “Insurance portfolio management should be driven by economic risk and return metrics, subject to capital constraints,” Etienne Comon, Managing Director at Goldman Sachs Asset Management, explained.

Solvency II places a number of capital constraints on the assets of an insurer, one of which is that they must hold sufficient funds against a range of risks. These so-called capital charges, help ensure the firm meets its Solvency Capital Requirement (SCR) and Minimum Capital Requirement (MCR). Breaching the former will trigger supervisory intervention, while a breach of the latter would likely mean the firm can no longer meet its obligations. The firm would then go into run-off or the regulator may look for a buyer for its liabilities.

The details for calculating the capital charges on different assets are set out in the Market Risk module in the standard formula. The treatment of bonds is specified in the spread risk sub-module. Because Solvency II currently takes a view that EEA sovereign bonds issued in own currency are risk-free, there is no charge applied to holding these assets.

John Roe, Head of Strategic Investment and Risk Management at Legal & General Investment Management, explains the implication of the charge under the current standard formula proposals. “If you have €1 billion of future liabilities and you own €1 billion of any European government bonds this will not, under the current wording, lead to a charge for the credit riskiness of those bonds. If you’ve also matched duration then, with the 0% capital charge on the credit risk, you would not need to hold any additional own funds to cover the risks associated with the assets.”

By comparison, if you held €1 billion of BBB rated corporate bonds against those same liabilities there could be a capital charge in excess of 25% and you could have to hold in excess of €250 million of own funds to protect against a potential drop in the value of the bonds.”

However, it is not only default risk that insurers must consider. “Sovereign risk is relevant to insurance companies’ solvency position because assets are marked to market,” Mr Comon said. “Therefore, any movement in government spreads and/or default risk has the potential to influence future solvency ratios through the variations in available capital, even if required capital is zero.”

Internal model firms

For firms planning on using an internal model, the discrepancy will already be captured in the internal model calculations.

Bruce Porteous, Head of Solvency II Regulatory Development, Standard Life, said, “Most large insurers, like Standard Life, use their own economic capital models and Solvency II internal models to assess these risks – these models capture the risks in these assets more appropriately.”

Mr Porteous believes the issue will only affect standard formula firms and will likely be resolved by the time the directive is in place. “We expect that it will be dealt with either by a recalibration of the standard formula before Solvency II is finally implemented, or via a supervisory capital add-on to the standard formula SCR post Solvency II implementation.”

It is also likely that some of the default and liquidity concerns will be captured in the move to mark-to-market accounting. A press release issued by Fitch Rating (24 November 2011) said, “[Mark-to-market] already goes some way to factoring in the risks insurers are taking of default on the bonds”.

The agency also said it did not believe the charge will be changed before implementation and instead suggested that a capital add-on may be applied by the regulator. “Capital increases, which can be added by regulators under Pillar II to reflect risk not captured in the standard formula, may also be imposed.”

But according to one estimate, currently only about 400 firms are applying to use an internal model. Based on figures from 2009, these represent less than two percent of all undertakings that will fall under the scope of Solvency II.

Solutions for the remaining 98%

So what of the remaining 98% of firms that will be using the standard formula to calculate the SCR?

One possible outcome of the mismatch is that insurance companies applying the standard formula will adjust strategies within the capital charges allocated under Solvency II to meet the requirements while actually creating a portfolio that reflects real market risk.

Mr Roe believes this could be a realistic outcome. “In my view, it is likely that insurance companies will adjust their total holdings to reflect their perception of real risk within the Solvency II constraints. So if you think the capital charge on corporate bonds is too high and accept that charges on sovereign bonds is unrealistically low you will adjust your portfolio so that in aggregate you have an amount of capital that represents the risk taken, rather than trying to arbitrage the rules,” he said.

Regulatory response

Both EIOPA and the European Commission reject the use of capital add-ons as a solution to the problem, as these should only be applied where the risk profile of an insurer deviates significantly from the underlying assumptions in the standard formula.

Professor Karel Van Hulle, Head of Unit Insurance and Pensions at the European Commission told Solvency II Wire, “Capital add-ons are an important tool in the Solvency II regime but they should be used only in exceptional circumstances and for certain situations. They should not be used systematically as a means of introducing capital requirements for sovereign bonds.”

The regulators say that ultimately the responsibilities for the management of risk lies with the firm and it should address this through the ORSA. Carols Montalvo, Executive Director, EIOPA, told Solvency II Wire that the current capital charges did leave firms using the standard formula exposed to market risk. But he insisted that “the solution for the firms should be part of the Solvency II framework, and firms are to target this issue through the ORSA.”

Mr Montalvo shrugged off suggestions that this could lead to more complex calculations or require additional resources that could amount to an internal model ‘through the back door’. “One of the main principles of ORSA is that firms should decide for themselves how to perform the assessment of the overall solvency needs appropriately, given the nature, scale and complexity of their risks,” he said.

“The assessment of the overall solvency needs does not necessarily call for a complex approach. Our recently launched consultation on the ORSA insists on the outcome expected, but leaves freedom to undertakings with regards to how to achieve it,” Mr Montalvo said.

The European Commission also views the ORSA as integral to managing sovereign debt risk and emphasised the importance of assessing exposure to credit risk.

Prof Van Hulle, said, “The regulatory capital requirements are only one element that firms should look at when managing their risks. Apart from specific quantitative requirements, insurers will have to have solid risk management in place. It is in particular expected that insurers undertake their own estimation of the credit risk to which they are exposed, including on central governments.”

He pointed to the recently issued Proposal on Credit Rating Agencies (CRA3) which makes explicit reference to the fact that all financial institutions, not only insurers, should carry out an assessment of their exposures to credit risk, “in particular, in order not to overly rely on external credit ratings.”

An internal model through the back door?

But the supervisory response is somewhat unsatisfactory, especially as it is not clear exactly how much additional work incorporating the risk into the ORSA will entail.

Raymond Bennett, Principal Advisor, KPMG said that while it was reasonable to expect firms to account for the sovereign bond risk discrepancy in the ORSA, what really mattered is defining the underlying assumptions.

“While the calculation of the default risk capital is fairly straightforward, the difficulty is in determining the appropriate assumptions to use to calculate the capital requirement (i.e. the 99.5th percentile). In the absence of clear guidelines from the regulators this could lead to a significant amount of work which may in some cases effectively equate to a partial internal model.”

The current charges are problematic in another way as well. Mr Roe warned that the treatment of the EU sovereign bonds, which is not in line with economic risk, would still leave insurers exposed to market risk if they took a purely rules based investment approach. “In a way treating all sovereign bonds as risk-free is not a realistic outcome because they do not reflect the real risk and you are not required to hold capital against that risk.”

If the treatment of the sovereign bonds in the standard formula results in the effective introduction of a partial internal model, and leaves firms holding insufficient own funds against default risk then Mr Bernadino’s ‘rethink’ is sorely needed. The question remaining is, what are the alternatives?

—

Part two explores counter cyclical measures and the implications of operating in an environment without a risk-free rate.