Part two: counter-cyclical measures and no risk-free rate Turmoil in the European government debt markets is calling into question the zero percent capital charge on European government bonds under Solvency II. This two part article explores how firms and regulators are handling the discrepancy between the charge and real default risk, and what life without a risk-free rate might look like.

Part one examined the implication of a zero percent capital charge on risk-free assets that are anything but. Part two looks at counter-cyclical measures and explores the implications of operating in an environment where nothing is risk-free.

The pitfalls of market consistency

The problem with regulation that reflects market prices is that it reflects market prices. When markets becomes very volatile, market consistent valuation can contribute to the volatility. For Solvency II, pro-cyclical behaviour is becoming an area of real concern. The European sovereign debt crisis is a painful reminder that regulators have to get it right on counter-cyclical measures. At times of extreme market stress, asset prices can deviate significantly from reflecting the underlying economic fundamentals. Instead, they reflect the fear, panic and self interest of investors.

Speaking at the EIOPA conference in mid November, Oliver Bäte, Member of the Board of Management of Allianz SE, said, “We all know that what we saw … in the last few weeks has nothing to do with underlying demand and control, and demand and supply but rather it is panic by investors and politicians that are driving this sovereign debt crisis.”

Mr Bäte stressed the importance of sovereign debt to the insurance industry. “We cannot fulfil our commitment to our customers if we cannot rely on governments to honour their debt, that we use to guarantee those commitments.”

Insurance companies continue to be heavily invested in European government bonds. According to the ECB’s Financial Stability Review (June 2011) the insurance and pension sectors jointly held about €1.1 trillion of debt securities issued by Euro area governments – an increase of €220 billion since the beginning of 2008. The figure represents 44% of the total holdings of debt securities for the two industries and 16% of their total financial assets. The relationship between government debt, the health of a country’s financial sector and its prospects of growth have become intertwined as the financial crisis deepens.

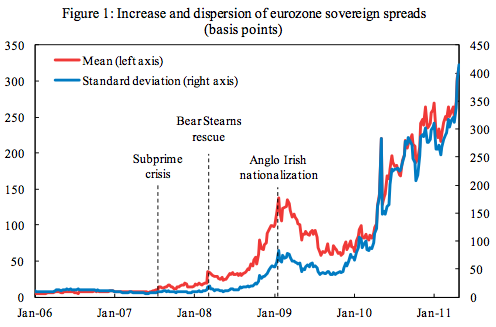

A recent IMF paper, The Eurozone Crisis: How Banks and Sovereigns Came to be Joined at the Hip argues that the bailout of Bear Sterns in 2008, and the subsequent nationalisation of Anglo Irish in 2009 were acceleration points in the interconnectedness of the financial sector and government debt, taking the crisis to a deeper and deeper level.

“The presumption that sovereigns would ride to the rescue of their domestic banking sector, linked the projection of a eurozone member’s sovereign debt to its domestic financial vulnerabilities: sovereign spreads now rose in response to perceived weakness of domestic banks,” the paper stated.

The fiscal strains on government balance sheets caused by the bailouts left them with less space to manoeuvre. According to the paper, this took the crisis to its current full-blown state. “Not only did financial sector stress raise sovereign spreads as before, but now sovereign weakness also transmitted to the financial sector.

Although spreads declined initially after the nationalization of Anglo Irish, the subsequent march upwards was spectacular, as was the country differentiation,” (see chart).

Introducing short-term volatility

But pro-cyclicality bites both ways. In the current economic climate it is easy to be caught up in doomsday-frenzy, yet the rule makers of Solvency II must consider market booms as well as busts.

As discussed in part one, while there are major concerns about the way the regulation treats European sovereign debt the likelihood of default is still very low. The treatment of counter-cyclical measures must not be clouded by what is happening now.

Matthew Elderfield, Head of Financial Regulation, Central Bank of Ireland, told Solvency II Wire that Solvency II was bringing us a long way towards an economic assessment of the underlying risks in the portfolio of insurance firms.

However, Mr Elderfield noted, “Experience has shown that market prices can undershoot or overshoot due to liquidity or other factors which cause short term volatility and that is not always clearly grounded on underlying credit fundamentals.”

The problem is that if short term volatility feeds directly into an insurer’s solvency calculations it can drive a downward or upward spiral.

“A key area of current discussion is how to design a mechanism in the capital calculations of Solvency II to provide for, if you like, a release valve for the impact of short-term volatility in sovereign debt valuation changes,” Mr Elderfield said.

“The challenge will be designing this framework in a way that embeds sufficient clarity and stability without hard-coding an arrangement that might incentivise perverse behaviour.”

Separating volatility from fundamentals

The solution will have to tackle the key obstacle of separating market volatility from economic fundamentals in the asset prices.

Mr Bäte said it was vital that the regulatory solution reflects real economics and does not propel market panic. “That does not mean that we ignore the risks, but we differentiate between the real risks and those that we are importing both through accounting volatility that is nonsensical and market volatility,” he said.

Looking at the ratings of individual countries rather than market prices is a possible step in this direction. According to Dan Morris, Market Strategist at J.P. Morgan Asset Management, “Because ratings agencies rely more on the underlying fundamentals and look at a longer term horizon, they can provide a view that is not as volatile as that reflected in credit default swaps spreads. It should then be possible to calculate a meaningful measure of how much of the price can be attributed to each factor.”

However, relying on rating agencies alone is problematic and unlikely to provide a sufficiently meaningful separation between real market price and short term volatility.

Solvency II counter-cyclical premium

Solvency II has a range of counter-cyclical tools at its disposal, including the Pillar I equity dampener, Pillar II extension of recovery period and the supervisory ladder of intervention.

The current EIOPA proposal to manage short-term volatility between asset and liability values is through the use of a counter-cyclical premium. This replaces the illiquidity premium used in QIS5 and will also include exposure to sovereign debt – something the illiquidity premium did not.

The current proposal will give companies the ability to apply the premium when market conditions are stressed – while EIOPA will retain the power to decide when these conditions occurs for individual markets. The industry has been opposed to this switch-on / switch-off mechanism for two main reasons.

First, market data has shown that while factors such as illiquidity increase during times of market stress, they are still present during more relaxed conditions (albeit at much reduced levels), and as such tend to tail in and out over time. Activating the counter-cyclical premium only at points of high market stress ignores these tail effects.

Second, not having a formulaic approach to the activation of the premium will make it difficult for insurers to include the premium in capital planning calculations. According to Dr William Coatesworth, Consultant at Milliman, “In its current form, the uncertainty around when the premium can be applied may leave companies unable to fully take account of the premium for pricing and capital management, effectively limiting its impact for such purposes.”

There are further concerns that giving EIOPA discretion in deciding when markets are in stress could become a political issue between countries, which would not wish to be declared as having markets in crisis.

Dr Coatesworth said, “This may result in significant delays between the time at which the market enters stress conditions and the point at which the counter-cyclical premium can be applied, further reducing the impact of the premium in it’s aim of reducing volatility.”

During his keynote speech at the EIOPA conference, Gabriel Bernardino, Chairman, EIOPA, said he did not support a complete formulaic approach and that it may not even be possible to design an adequate one.

“We should not pretend to play God and believe that we can decide in advance how the next crisis will look,” he said. “Nevertheless, on top of a more flexible approach, I would support the definition of a set of clear criteria and indicators that should be constantly monitored by EIOPA and that would lead to a decision on the application of the counter-cyclical premium by EIOPA on a European basis when certain defined thresholds would be exceeded.”

The risk free rate

Whatever solution is found to address extreme market volatility, regulators must consider the treatment of sovereign bonds as a special case. Because sovereign bonds are used to determine the risk-free rate, any change to the zero percent capital charge on them would be akin to an admission that the system no longer has a risk-free rate.

Already insurance firms and other investors are seeing the traditional risk and return equation (i.e. higher risk = higher return) being eroded. Peter Praet, Member of the Executive Board of the European Central Bank, said that the reappearance of credit risk in the sovereign debt markets was making it difficult for insurance companies who were already struggling with persistent low yields on risk-free assets.

Speaking at the 6th European Pension Funds Congress, Mr Praet said, “Now they discovered that low yield is also attached to credit risk and market price risk. So here the response of course is that public finance has to be in order. It is very important in any society that sovereigns remain of very good quality in the whole financial system.”

Mr Praet highlighted the importance of the risk-free rate to the economy. “Any course on money and banking will start with the risk-free rate, the yield curve and government debt. And that is the sort of benchmark in our economies to fix the prices.”

“If there are doubts about the credit quality of this benchmark, all your pricing system gets jammed and this is the situation we get here in a number of countries especially in the Euro zone. So it is very important not only for the good sake of public finances … but also for the good functioning of our financial system because other things are fixed around them.”

“Maybe later we will get other benchmarks but for the time being it is quite difficult to replace the government yield curve as reference pricing system,” he added.

What if nothing is risk-free?

The economic effects of operating without a risk-free rate are explored in the somewhat dramatically titled paper, Into the Abyss: What If Nothing is Risk Free?, by Professor Aswath Damodaran at the Stern School of Business, NY.

The paper, which also includes an interesting discussion on the use of ratings agencies to evaluate sovereign default and alternatives to a risk-free rate, considers the effect on investment as well as corporate finance.

It argues that a lack of a risk-free investment will make risky investments appear even more risky to all investors. It could also result in less diversification in the absence of a risk-free rate for investors to fall back on.

“Having an investment that is risk free is critical not only for financial modeling but also for investor behavior and corporate financial analysis. From a measurement standpoint the return on the investment (the risk free rate) provides the basis for computing expected returns on risky assets and the presence of a riskless asset also changes investment, financing and dividend policy at firms.”

Some, however do not think this will have a material effect on asset management. According to Mr Morris, “Not having a risk-free rate is unlikely to change investors’ approach dramatically. Investors will still want to hold the least risky asset available but at some point some of the capital requirements could rise.”

But the paper does raise an interesting point that is relevance in the overall discussion about the effects of regulation on markets in times of high volatility. “Investors may not consciously think about the riskless asset but having one provides psychological solace that in times of crisis, they will have a safe haven for their savings. Not having a riskless investment can therefore be unsettling for investors and can have significant consequences for the pricing of all risky assets.”

Tread lightly

There are a number of obvious reasons why no regulatory system can openly declare its government bonds to no longer be risk-free and Solvency II is unlikely to be a trailblazer in this respect. The panic such an open declaration would unleash would be difficult to comprehend and its effects potentially devastating.

Given the interconnectedness of the financial sector and growth potential – largely brought about by government bailouts – regulators must tread ever more carefully with counter-cyclical measures.

Related Articles:

Risk-free or not? Solvency II grapples with sovereign debt

Risk-free or not? Solvency II grapples with sovereign debt, part two