ANALYSIS

Solvency II has been in force for over two years. Its effects have yet to be fully felt by insurance companies, customers, regulators, and capital providers. However a number of impacts well beyond the regulatory solvency framework are already evident. In this research note Laurent Rousseu, Deputy CEO of SCOR Global P&C, discusses the value of the Solvency II disclosures for reinsurers.

Solvency II and the value for reinsurance

As a reinsurer, we view the use of this newly accessible information from the Solvency II public disclosures as key in three different areas: individual client information, market benchmarking and pricing analysis, and increasing reinsurers’ ability to deliver more tailored solutions to their clients.

Individual client information

Individual client information: for fundamental “Know Your Client” purposes, feeding and enhancing the reinsurance underwriting process: The underwriting process should be fed by as broad an information stream as possible, to enable reinsurers to reliably assess their clients’ risk appetite and risk transfer needs, both of which translate into their reinsurance buying structure and pattern over time. While reinsurers already have information on certain risks and programmes that goes well beyond what is provided in the Solvency II disclosures, the SFCRs provide a useful holistic framework, including information and data on parts of the business that may never have made it to the reinsurance market – whether due to deliberate non-disclosure or simply because the information was not produced before, at all or on a regular basis. This information can take the form of either qualitative disclosures, such as those found in the SFCRs on system of governance or risk profile, or quantitative data as presented in the QRTs. While the quantitative data gives valuable information on business performance and balance sheet solidity, the qualitative disclosures provide the background on the risk management culture and control framework. The interaction of these two sources of information can provide important insights into the management of a client’s business.

Market benchmarkingand pricing analysis

As time series become available with annual releases, public QRTs will become key sources of information for risk assessment and valuation or pricing purposes. This is particularly true for Line of Business disclosure (premiums and reserves), which is provided gross and net of reinsurance for individual (“solo”) entities and groups, leading to market and line of business benchmarks built from a more complete and comparable data set than previously. Outliers will therefore become more easily identifiable, leading to a better relative positioning analysis of each insurer in a given market.

Delivering moretailored reinsurance solutions

Insurers’ discretion when disclosing information to their reinsurers will be reduced as SFCRs will disclose information on portfolio subsets that might be unknown to external capital providers (reinsurance, debt, equity, etc.). This increased disclosure is an additional incentive for insurers to be as transparent as possible to their stakeholders, and a tool for these stakeholders to be more autonomous when providing capital and earnings’ volatility management solutions to insurance companies. Reinsurers will potentially be able to propose solutions for their clients proactively, based on a wider information set than that contained in broker information packs.

Deep dive into the QRTs of selected insurance markets

We illustrate the above points by providing the standard analysis we produce on insurer and market benchmarks using a number of Nordic insurers and markets. The publication of QRTs (both for solo entities and Groups) as part of the SFCRs allows all stakeholders to analyse the balance sheet structure and P&L performance of all insurance companies, and to benchmark them against each other. This can be done within a single market, or by comparing similar companies across markets. The information provided can generally be divided into 3 different types:

- Solvency position and balance sheet structure

- Operating performance

- Approach to reinsurance

Solvency position and balance sheet structure

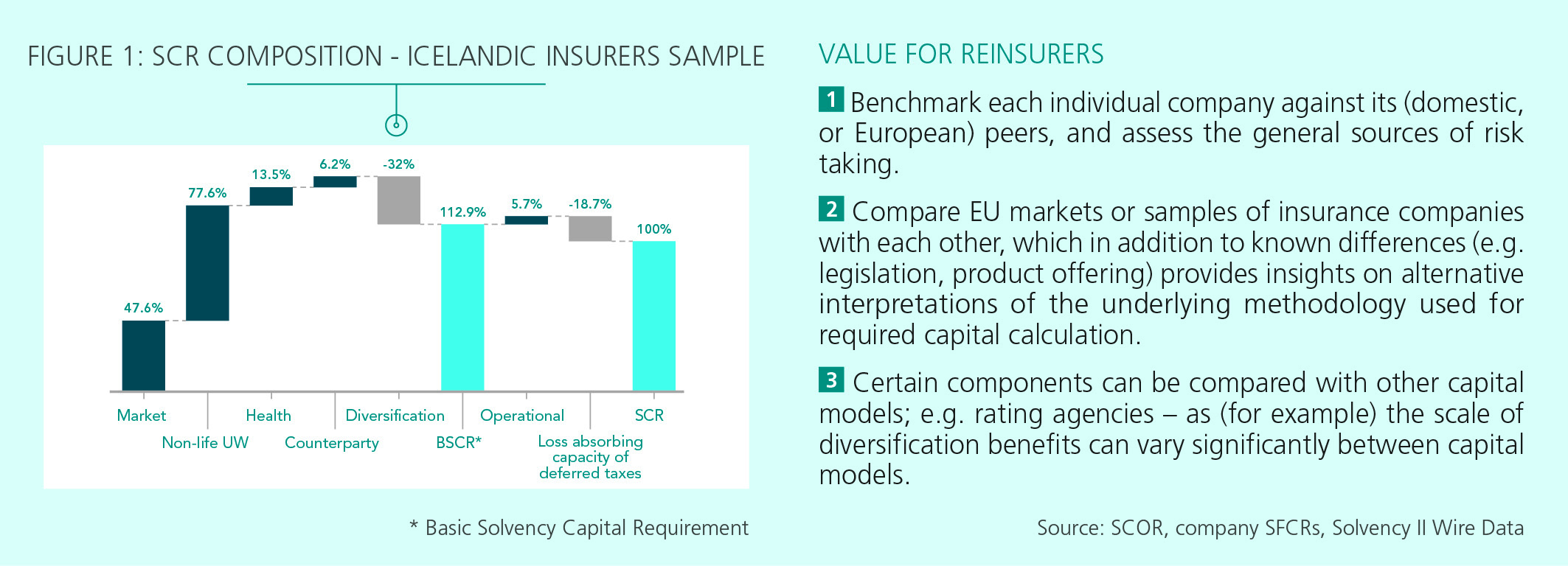

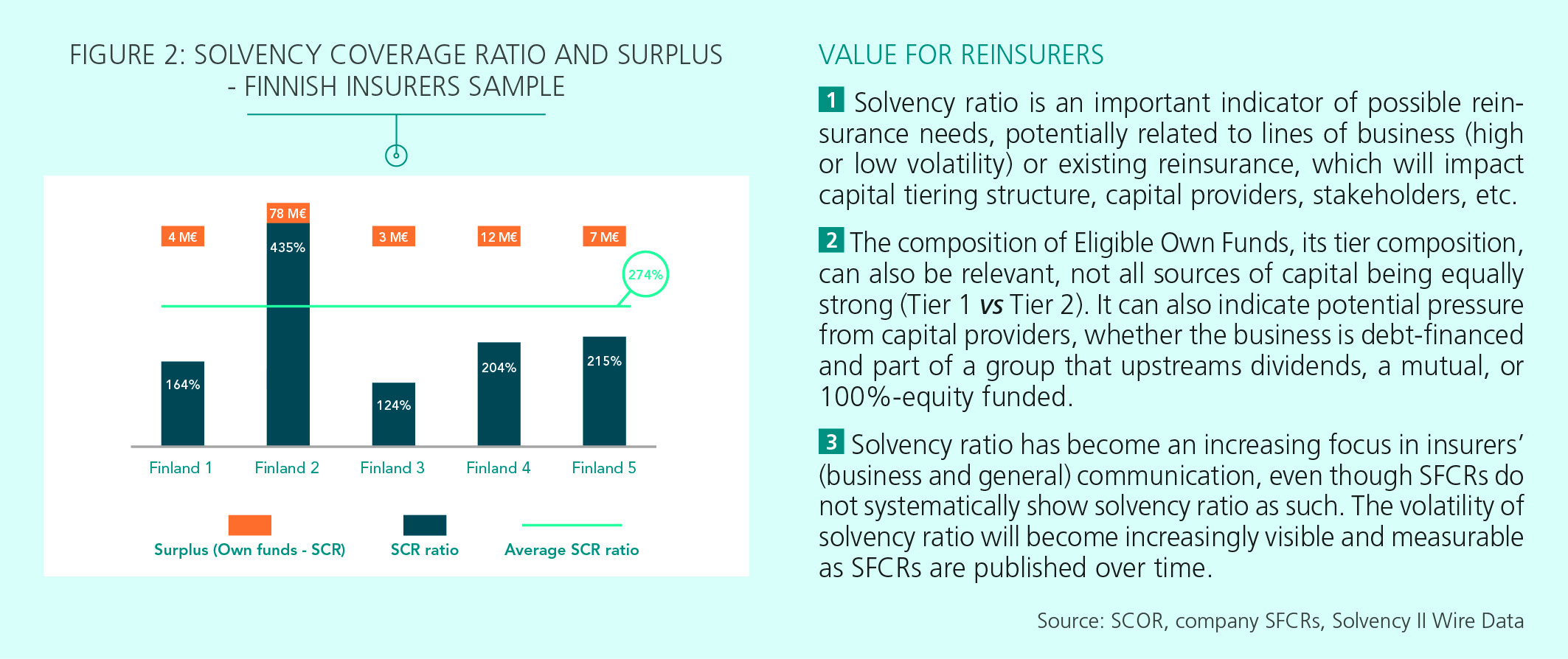

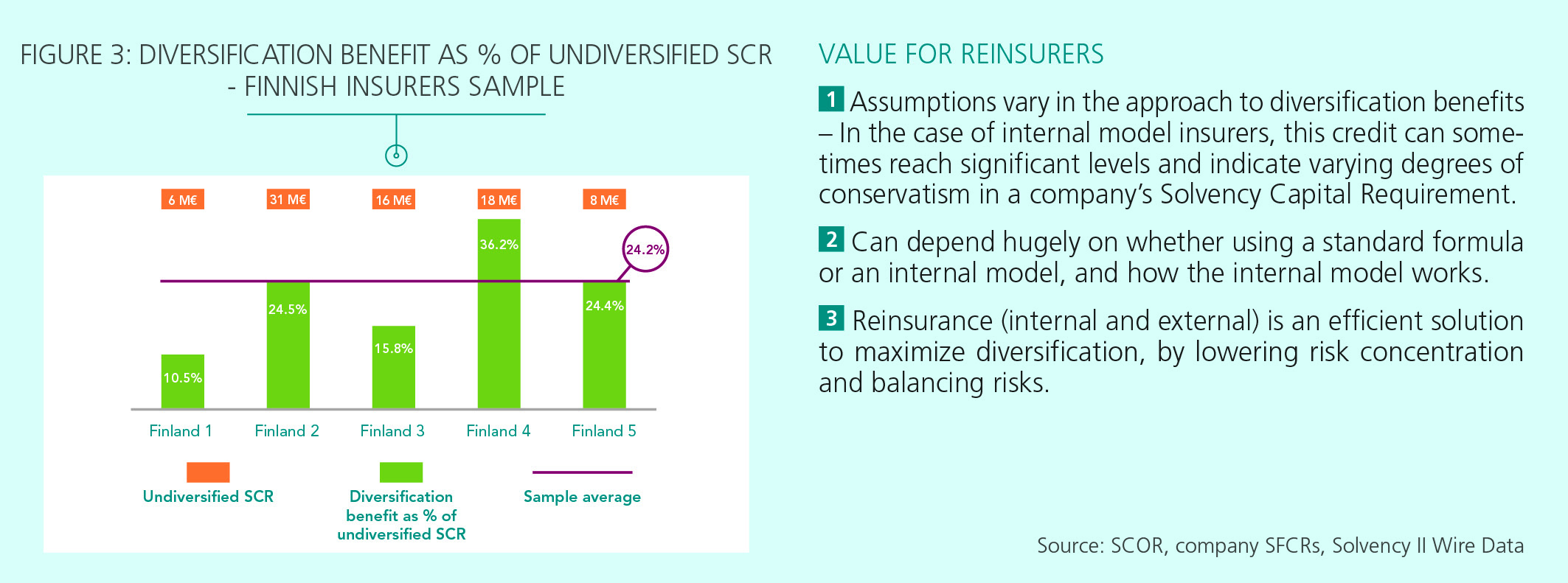

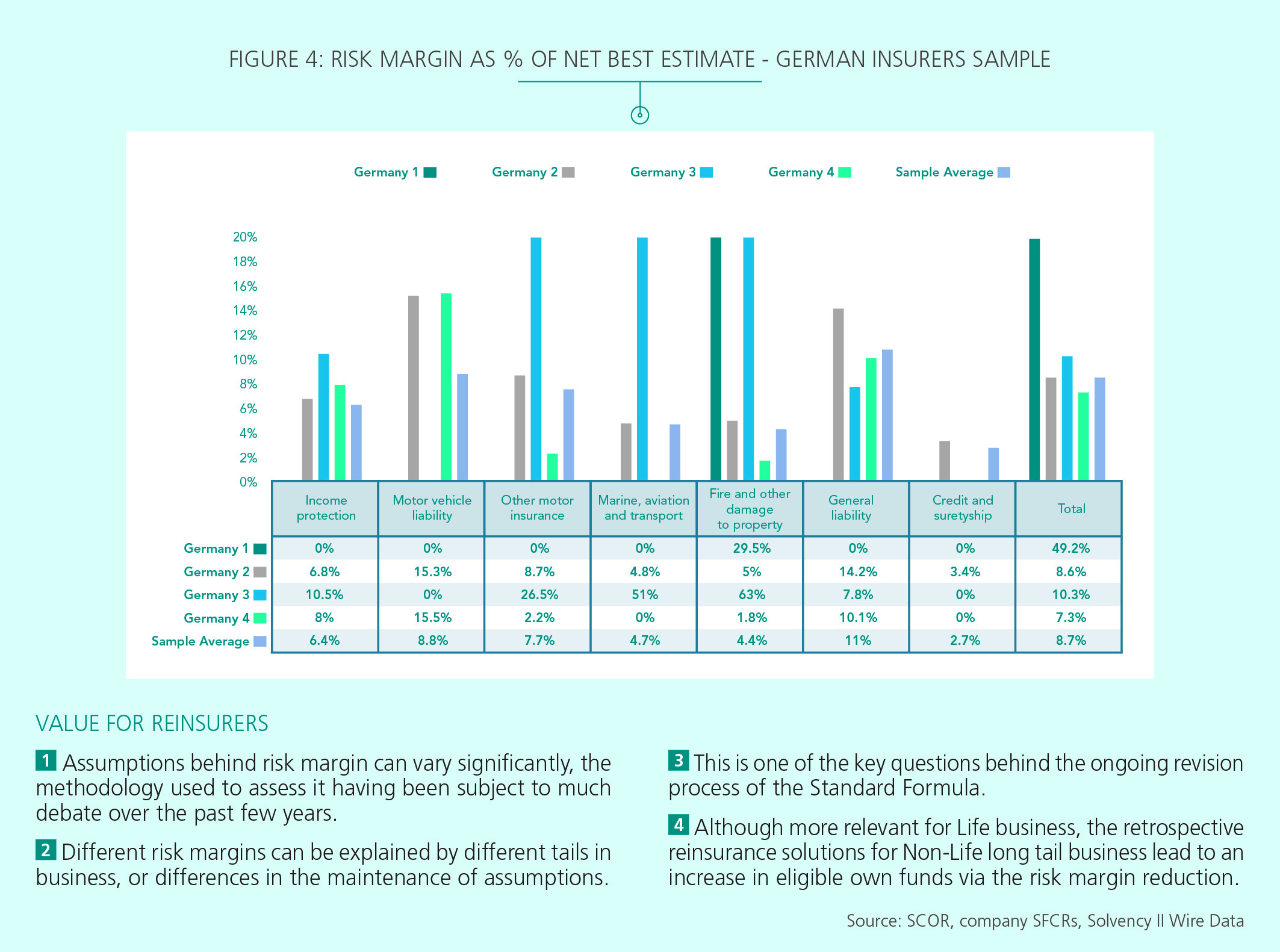

Balance sheetinformation can be useful to reinsurers in several respects. Generally speaking, it can help reinsurers to better understand an insurer’s situation and robustness, the balance sheet being the result of its history. The balance sheet is the starting point to understand an insurer’s risk appetite: an economic approach would imply that the stronger the balance sheet, the higher the risk appetite should be (even though it is often not the case). Following from both points above, reinsurance solutions can make an insurer’s balance sheet stronger, or optimized. Reinsurance “alternative solutions” focus on creating eligible own funds, or alleviating capital needs generated by the balance sheet structure. The following four charts illustrate the ways in which the disclosures can be used to analyse the solvency position and balance sheet structure of individual insurers as well as cross-market segments. Figure 1 shows details of the SCR composition. Figure 2 demonstrates how reinsurers can benchmark solvency coverage ratios and surplus information Figure 3 examines the diversification benefit as a proportion of the undiversified SCR. Figure 4 examines the risk margin as a proportion of net best estimate liabilities and highlights some of the benefits for reinsurers.

Operating performance

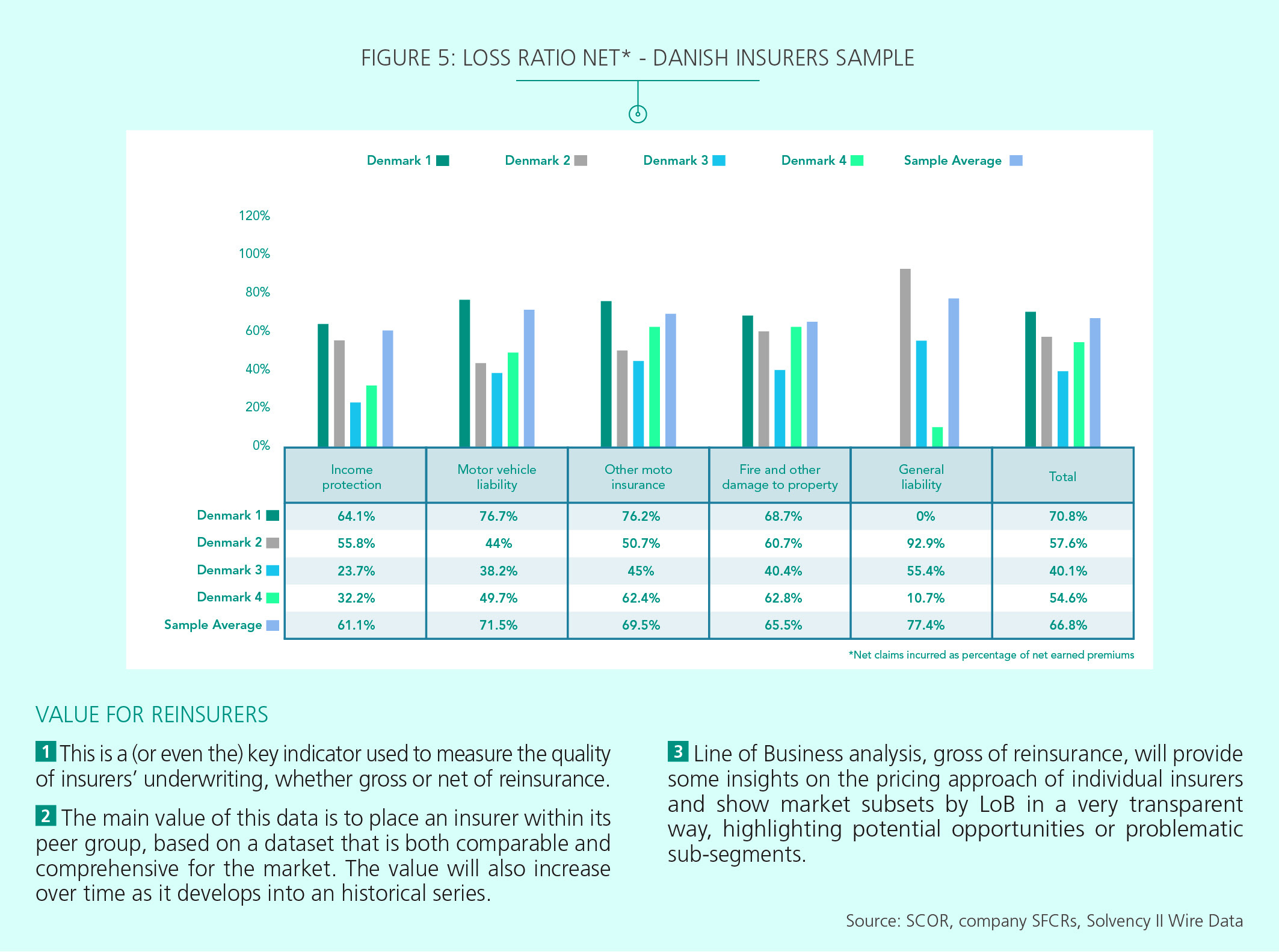

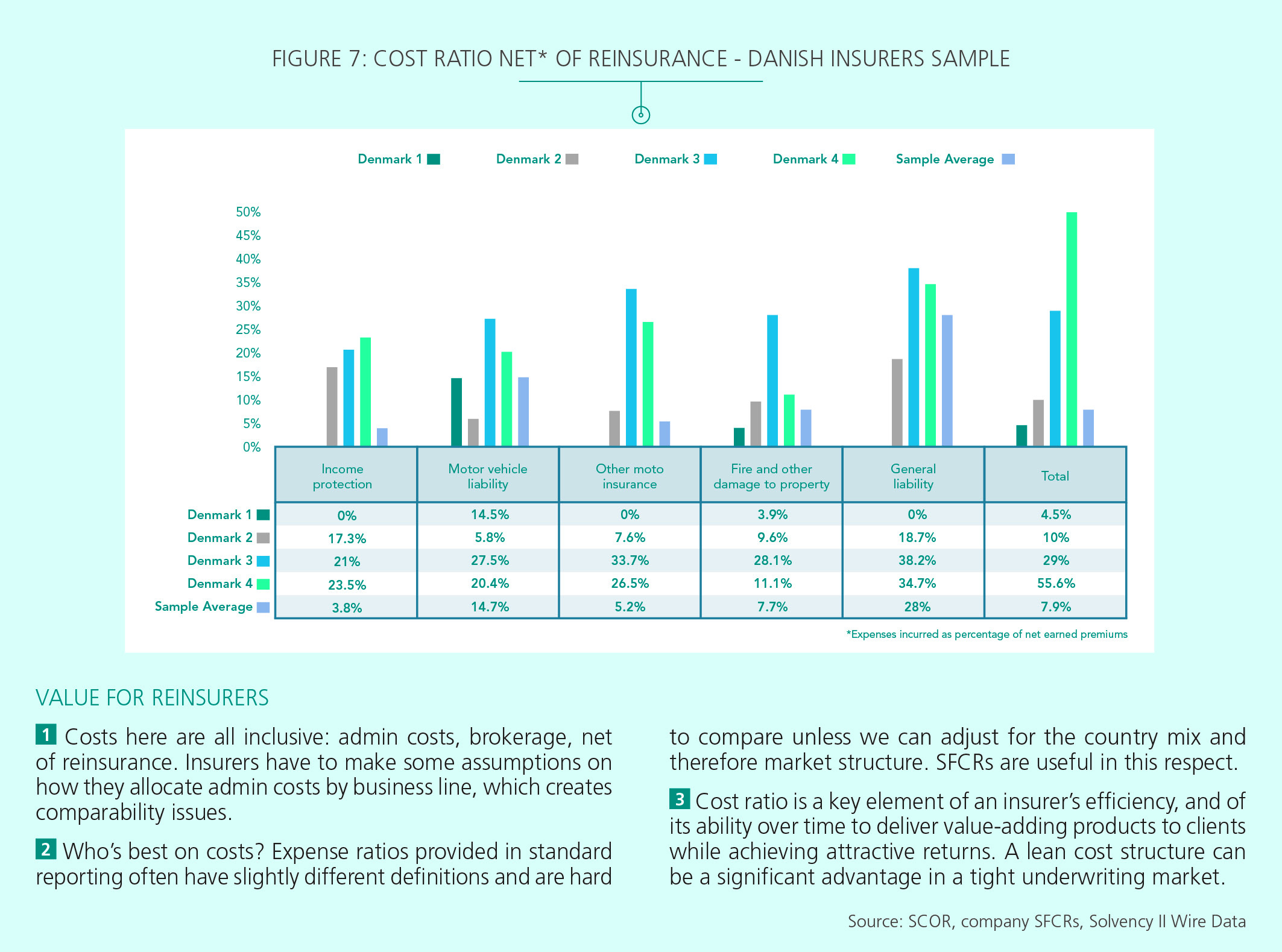

There is a general perception that, over time, the interests of reinsurers and insurers align, and should converge as both carriers share their fortunes. It is therefore key for reinsurers to fully understand the top line growth and profitability trends of their clients, whether at a business line or aggregate level. The operating performance analysis that can be derived from public QRTs range from business mix analysis to underwriting performance and operational efficiency. Just as with balance sheet analysis, reinsurance underwriters should increase their financial skills to analyse this Profit & Loss Account data in a way that is useful to the underwriting process. The following charts demonstrate how operating performance can be evaluated and derived from the Solvency II public disclosures.

Approach to Reinsurance

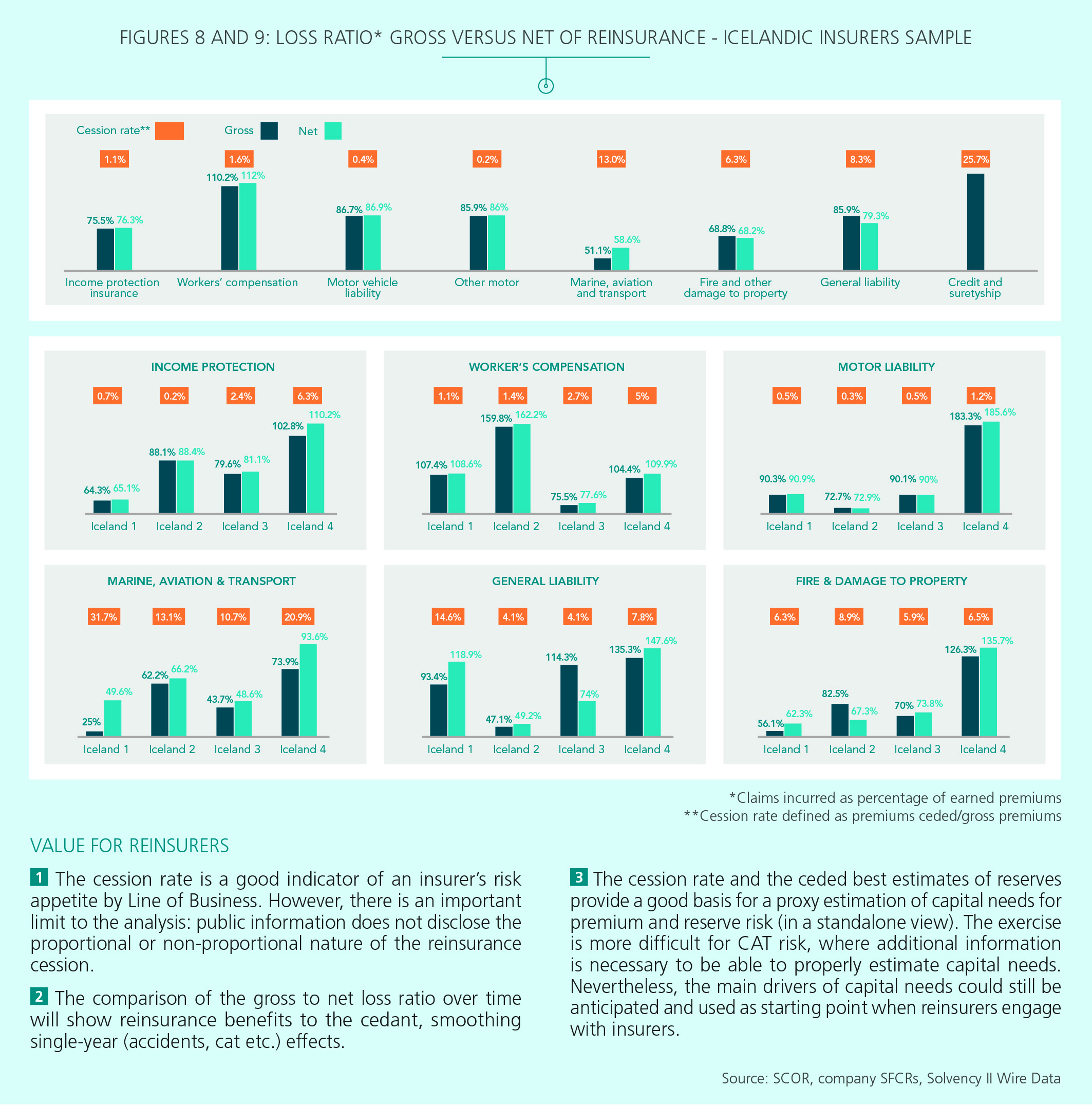

The Solvency II public QRT disclosures are of course less detailed than insurers’ reinsurance submission packs, which are prepared with the assistance of brokers for reinsured business lines. But QRTs do provide potentially interesting insights on less or non-reinsured lines of business, whether for a given market overall (provided the reinsurance buying structure is homogenous between insurers) or for single companies. Up to now, reinsurers have been restricted by the financial and risk information available beyond that provided by brokers. However, the increasing scope of public regulatory information creates opportunities to tailor solutions to specific insurers. The following figures illustrate how the disclosure can bring value to understanding and enhancing an insurer’s approach to reinsurance.

Conclusion

As regulatory pressure continues, it will become increasingly important for reinsurance underwriters to combine financial and underwriting skills, in order to prepare better for the future of the (re)insurance industry and the needs of their clients. — The author is Deputy chief executive officer of SCOR Global P&C. Views expressed are the author’s own. SCOR Technical note #43 – April 2018 ‘What should we make of European Insurers’ Solvency II Disclosures?‘ can be accessed here.